Further protection for the taxpayer can be good policy, but lawmakers must ensure there are no unintended consequences along the way.

The Iowa Legislature is considering a joint resolution that would establish protections for Iowa taxpayers in the state constitution. Senate Study Bill 1207 and House Study Bill 232 propose two amendments. The first would require two-thirds of both chambers of the legislature to approve any income tax increase. The second would ensure the Taxpayer Relief Fund is used only for the purpose of “reductions to income tax rates, sales and use tax rates, or property taxes.”

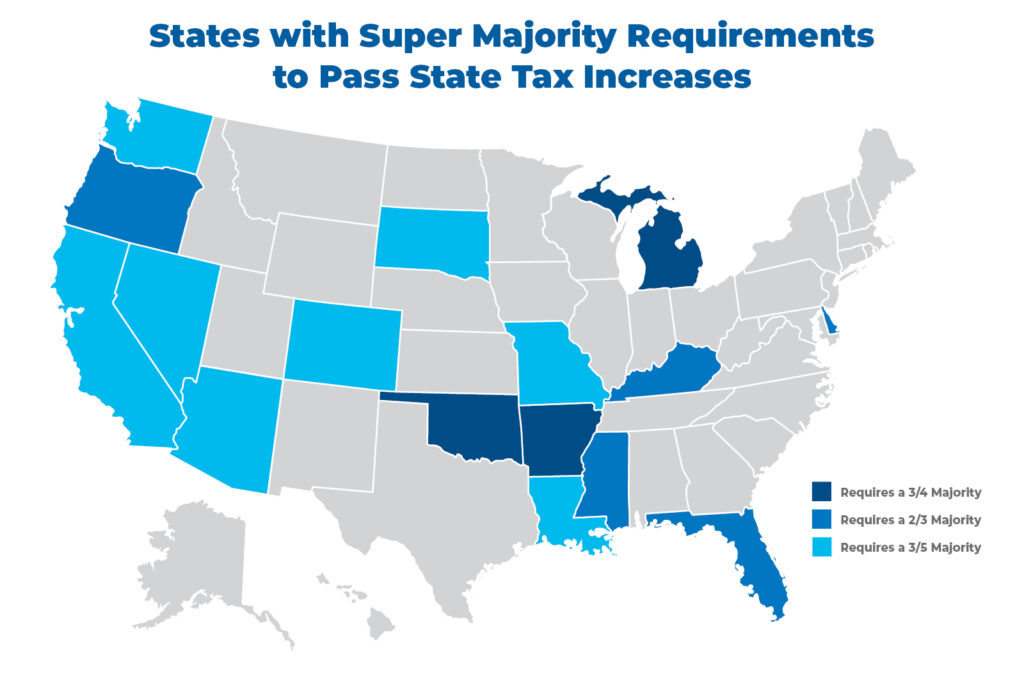

The proposed constitutional protections for Iowa taxpayers are noble, especially after last year’s historic tax reform, which when fully implemented will create a flat 3.9 percent income tax rate. Establishing a two-thirds requirement to pass an income tax increase is a strong protection for taxpayers, though one that would not be unique to Iowa, as illustrated on the following map. 16 states have some form of super majority requirement for tax increases, including seven states with that protection enshrined in their constitution.

While requiring a supermajority to pass an income tax increase is a good taxpayer protection, policymakers should proceed carefully with the Taxpayer Relief Fund proposal. The original intent of the Taxpayer Relief Fund was to use any surplus budget dollars, which are an overcollection of income taxes, to provide income tax relief; it was never intended to reduce sales or property taxes.

In fact, the legislature is currently considering an income tax reform measure that would continue reducing the income tax rate until it reaches a flat 2.5 percent in 2028. Beyond that point, the proposed legislation would utilize the Taxpayer Relief Fund, which would be renamed the Income Tax Elimination Fund, to gradually eliminate the individual income tax altogether.

The Taxpayer Relief Fund was born in 2011 as the Taxpayer Trust Fund, which the legislature enacted to capture excess revenue on behalf of income tax payers. Lawmakers believed it to be the best way to ensure surplus tax collections ended up back in the pockets of the people who paid them, rather than creating incentive for more state-level spending. At the time, the fund was capped at $60 million, and Iowans received credits on their state tax returns each year there was a balance within that fund.

A 2018 reform renamed the Taxpayer Trust Fund as the Taxpayer Relief Fund and removed the $60 million cap. Furthermore, taxpayers no longer received an automatic return of the excess revenue. Rather, the legislature’s mandate is now to return those dollars through tax relief measures of its choosing. Along those lines, sales and property tax reductions are fine things to consider, but the proposed amendment could be improved to ensure the Taxpayer Relief Fund eliminates the income tax altogether before flowing toward sales or property tax relief.

The Taxpayer Relief Fund’s current balance of $2.7 billion is projected to increase to $3.5 billion by fiscal year 2024. The large pool of money creates temptaions for policymakers to dedicate it to new spending programs or direct it to local governments through property tax relief. Taxpayers should consider new spending to be out of the question from the start, and they should be concerned that using the fund for property tax relief may only deliver temporary results. Diverting Taxpayer Relief Fund dollars to property tax relief could simply be another instance of the state subsidizing local government spending growth.

The crucial point no one should ever lose sight of is high property taxes are driven by local spending. Failing to address that cause would put the Taxpayer Relief Fund in danger of becoming merely a dedicated funding source for local budgets. True and meaningful property tax relief will only come about through local government spending limits and systemic changes to Iowa’s property tax system.

Putting protections for taxpayers into the state constitution — and out of the hands of any given legislature’s whims— can be good policy. While both proposals offer more protection than exists today, it will be important for lawmakers to ensure there are no unintended consequences along the way.

Print a PDF

Print a PDF