This article was published in National Review.

Iowa policymakers have an opportunity to allow taxpayers to keep more of their hard-earned income, make the state more competitive, and provide protection that will benefit taxpayers for generations.

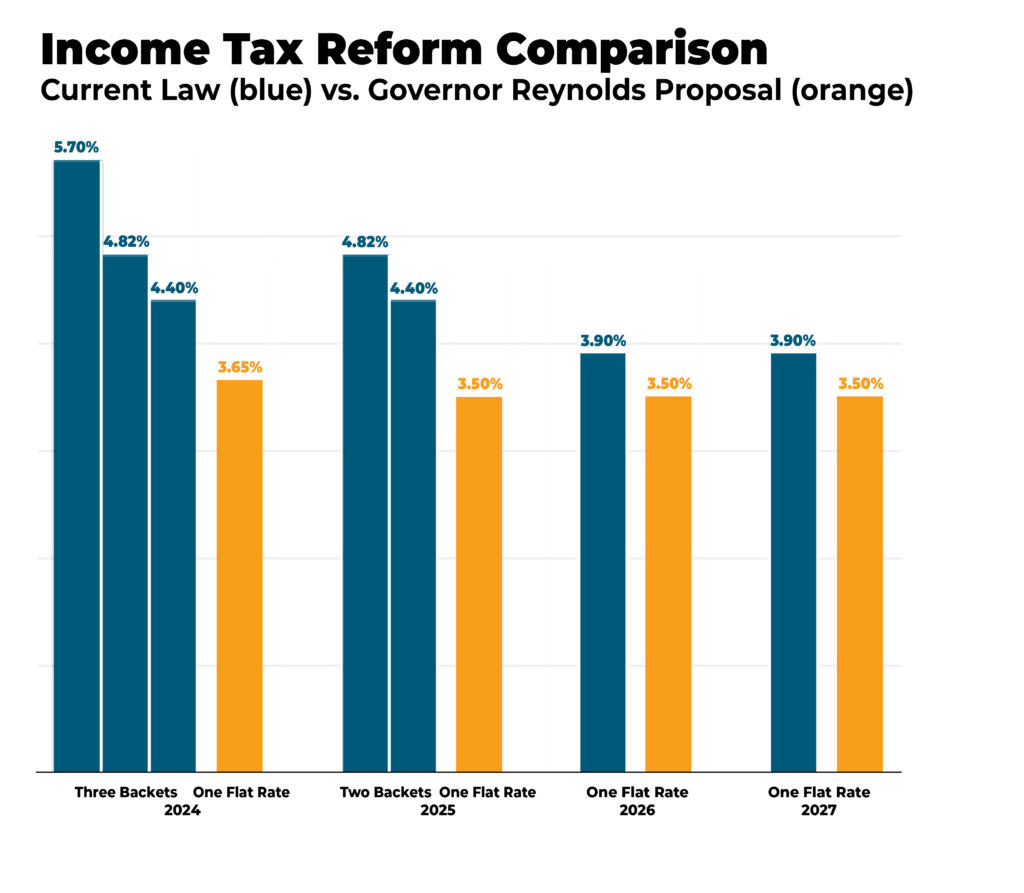

In 2022, Iowa confirmed its position as a leader in the state flat-tax revolution by phasing out the nine-bracket progressive income tax and replacing it with what will ultimately be a 3.9 percent flat tax in 2026. As a result of conservative budgeting and pro-growth tax reforms, Iowa’s fiscal foundation is strong. This provides a historic opportunity for Iowa to not only make the tax code more competitive but enact permanent tax relief. Governor Kim Reynolds and the Iowa House and Senate have each proposed significant tax reform measures that would put Iowa on the map as a leader in economic competitiveness for years to come.

Putting commonsense limits on spending growth is the foundation for successful long-term tax reform. Over the past several years, Iowa has enjoyed a budget surplus, ending fiscal year 2023 with a $1.83 billion surplus. Iowa’s reserve accounts are filled at their statutory maximums (over $900 million). The surpluses have also fueled enormous growth in the Taxpayer Relief Fund, which has a current balance of $2.73 billion and is projected to increase.

In short, this means that Iowa is still collecting too much from taxpayers. As Governor Reynolds put it, “Let me be absolutely clear: the surplus does not mean that we aren’t spending enough; it means we’re still taking too much of Iowans’ hard-earned money.”

As a result, Gov. Reynolds is proposing to accelerate the rate of income-tax reductions and even lower the flat tax. to 3.65 percent this year. The rate would further be lowered to a flat 3.5 percent in 2025. This would amount to a $3.8 billion savings for taxpayers over the next five years.

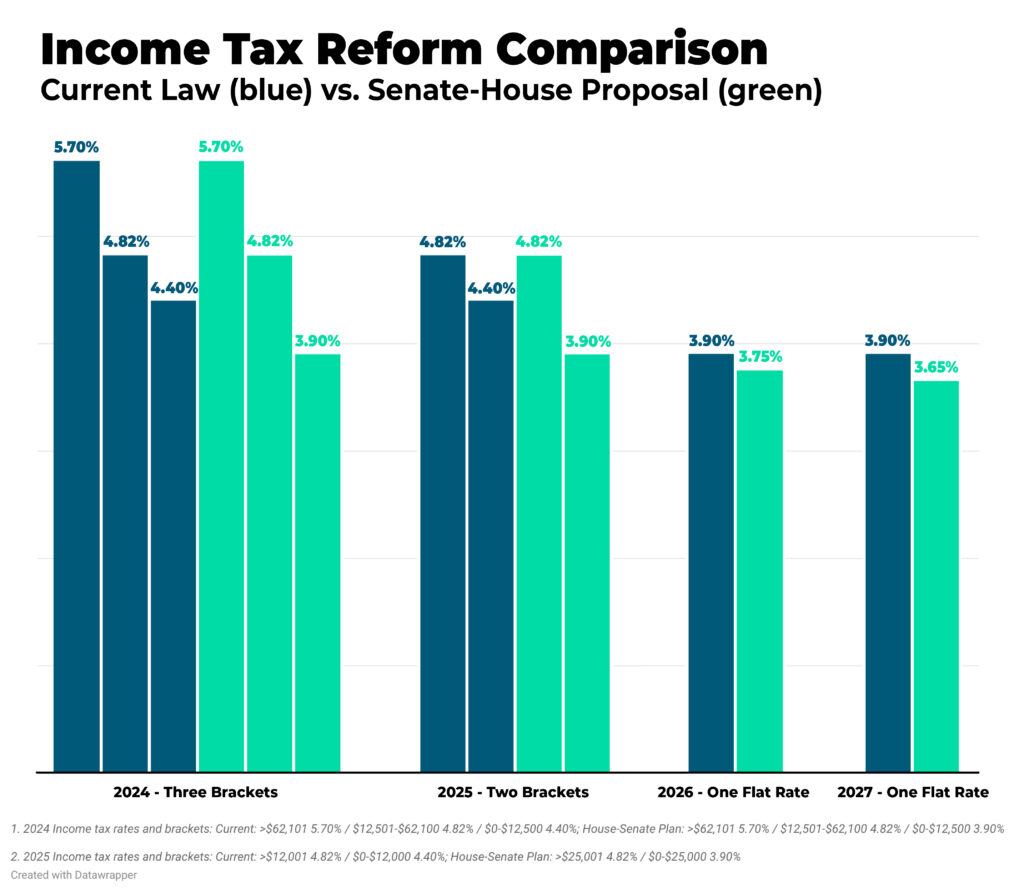

State senator Dan Dawson and state representative Bobby Kauffman, who both serve as chairs of their respective chambers’ Ways and Means committees, have also introduced an important tax reform proposal. The proposal similarly calls for accelerating income tax rate reductions, but it also creates a path that will not only continue to lower the rate, but eventually eliminate the income tax altogether.

Under the Dawson-Kauffman proposal, income-tax rates would be gradually reduced until a 3.65 percent flat rate is reached in 2027. In addition, to accelerate rate reductions, the proposal creates a new mechanism that utilizes the accumulation of budget surpluses to slowly eliminate the income tax.

This innovative idea would transfer dollars from the Taxpayer Relief Fund into a new trust fund that will be managed by (but separate from) the Iowa Public Employees Retirement System (IPERS). As that trust fund grows, earnings from the fund would be used to replace general fund revenue that is being slowly ratcheted down by decreasing income tax rates. As a safety measure to ensure budget stability, future rate reductions would only occur in fiscal years when several fiscal benchmarks are met. This approach honors the original intent of the Taxpayer Relief Fund by ensuring that those dollars be used for income tax relief and not additional government spending.

Dawson and Kauffman are also proposing two important constitutional amendments that would serve as additional taxpayer protections. The first would require a two-thirds supermajority vote of the legislature to increase taxes, and the second would constitutionally protect the flat tax.

Governor Reynolds and legislative leaders have proposed significant pro-growth tax reform measures that would benefit taxpayers, create opportunity, and make the economy more competitive. Going forward, both of these proposals will be debated, and a crucial factor will be the continual necessity to restrain spending growth.

Already critics are arguing that, if further income tax cuts are enacted, Iowa will be headed for a fiscal crisis. Nothing could be further from the truth. These critics ignore the failed tax and spend policy lessons from states such as Minnesota and Illinois. These fellow Midwestern states have increased spending and taxes to far higher levels and are now confronted with fiscal crises. Minnesota, after historic spending and tax increases, could soon be confronted with a budget deficit. Illinois, which has been in a continual fiscal crisis, is facing a potential $891 million deficit. This is an unfortunate pattern that is taking place among many progressive states , including New York and California. The spend and tax agenda does not work.

Further, an exodus of businesses and individuals is taking place from high tax states across the country, as the ALEC Rich States, Poor States report documents annually. This outmigration effect suffered by fiscally profligate states only compounds the loss of economic vitality — and, ultimately, tax receipts.

Over the last several years, Governor Reynolds and Iowa lawmakers have followed a successful fiscal conservative agenda. As Iowa’s house speaker pro-tem, John Wills, put it, “I look forward to continuing the great strides Iowa has made to protect hardworking taxpayers. By investing our historic surplus to buy down and eventually eliminate the income tax, we can responsibly balance the need for core government services and the need to make Iowa more competitive for job growth.”

This year presents a historic opportunity for policymakers to enact significant pro-growth tax reform that will not only allow taxpayers to keep more of their hard-earned income and make the state more competitive but also create constitutional protections that will benefit taxpayers for generations.

Print a PDF

Print a PDF