President Herbert Hoover Understood the Cause of the Great Depression

By John Hendrickson

Source: Herbert Hoover Presidential Foundation

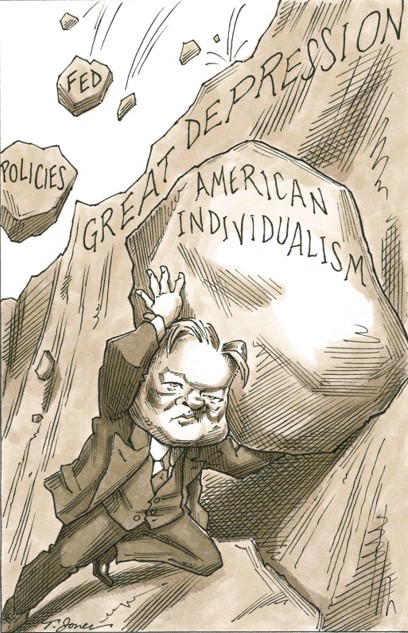

Former Federal Reserve Board Chair Ben S. Bernanke wrote that “to understand the Great Depression is the Holy Grail of macroeconomics.”[i] The cause of the Great Depression is not the only source of debate. Debate exists over why the Depression lasted such a long time and how it was eventually resolved. President Herbert Hoover argued that the origins of the Depression resulted from a combination of the collapse of international finance and the monetary policy of the Federal Reserve. “The central difficulty during my term as President was, obviously, the world-wide ‘Great Depression,’” wrote Hoover.[ii] It was the collapse of the international economy that Hoover argued was the major driver of the Depression. Hoover was correct when he argued that both factors contributed to the Great Depression. Nevertheless, what made the Depression worse in the United States was the direct result of the Federal Reserve’s monetary policy responding to both internal and external economic forces.

Source: Hoover Institution

Hoover argued that the “Great Depression did not start in the United States.”[iii] Hoover was not arguing that the United States economy was not suffering from some serious problems. “To be sure we were due for some economic readjustment as a result of the orgy of stock speculation in 1928-1929,” stated Hoover.[iv] Hoover reasoned that a combination of monetary policy and the collapse of international finance was the cause of the Depression. In addition, he argued that it was the collapse of the international economy which turned a correction into a severe Depression.

“In each case, domestic and global imbalances contributed to a global crisis,” wrote economic historian Michael Lind.[v] The Great War (World War I) provided the foundation for the international economic collapse. Charles Morris, an economic historian, argues that the Great Depression was a “world phenomenon with roots in World War I.”[vi] Further, Morris agrees with Hoover that even though the economy during the 1920s was successful it was showing signs of “overheating.”[vii]

Some of the signs of economic overheating included the reckless speculation in the market, over production, and the ongoing crisis in agricultural commodities. “By the time of the stock market crash, it was due for a major, possibly a nasty, correction,” wrote Morris.[viii] Hoover argued that these problems would have resulted in comparable situation as past economic corrections in American history.[ix]

Hoover was referring to the boom-and-bust business cycle, which had occurred throughout the nation’s history. Prior to the Depression the American economy went through a series of economic downturns in 1819-1820, 1839-1843, 1857-1860, 1873-1878, 1893-1897, and 1920-1922.[x] The late economist Hans F. Sennholz argued that what each of these economic downturns had in common was the federal government “generated a boom through easy money and credit, which was soon followed by the inevitable bust.”[xi]

The United States was hit hard by both the easy credit monetary policy of the Federal Reserve during the 1920s and the collapse of international finance. “The whole financial and economic structure of Europe collapsed at this time as a result of delayed consequences of the First World War, the Versailles Treaty, and internal policies,” wrote Hoover.[xii]

In the aftermath of World War I the Allies had required Germany to pay substantial reparations, and, in the aftermath, the German economy was in shambles. The United States during the 1920s tried to organize an effort with the Dawes and Young Plans to negotiate the high reparations payments, but the collapse of European economies had a substantial impact on the world economy. This included the suspension of debt payments and the abandonment by some European nations, especially Great Britain off the gold standard.[xiii]

Source: Our Iowa Heritage, Ding Darling cartoon, 1931

Hoover was committed to the gold standard and as Michael Lind wrote “when European nations abandoned this it limited America’s flexibility in monetary policy.”[xiv] Economic historian John Steele Gordon argues that the Federal Reserve’s attempt to “defend the dollar and maintain the gold standard” create substantial problems.[xv] Gold was being repatriated back to foreign banks and as Gordon notes this led the Federal Reserve in response to raise interest rates, which resulted in “cutting the money supply, causing an already severe deflation to become much more severe.”[xvi]

Hoover argued that the collapse of international finance added “fuel to the fire” and he added if that had not occurred the “domestic difficulties standing alone would have produced no more than the usual type of economic readjustment which had reoccurred at intervals in our history.”[xvii] Hoover described the collapse of European economies as an “economic hurricane.”[xviii]

As a result, the Federal Reserve had to respond by not only addressing market speculation, but also the impact of collapsing European economies. The late economist Milton Friedman argued that the Depression was made worse by the Federal Reserve’s monetary policy, which not only resulted in deflation, but also contributed to a series of bank panics.[xix]

Gary Richardson, an economist with the Federal Reserve Bank of Richmond, described the policy of the Federal Reserve in attempting to address both the easy credit of the 1920s and the drainage of gold when he wrote:

An example of the former is the Fed’s decision to raise interest rates in 1928 and 1929. The Fed did this in an attempt to limit speculation in securities markets. This action slowed economic activity in the United States. Because the international gold standard linked interest rates and monetary policies among participating nations, the Fed’s actions triggered recessions in nations around the globe. The Fed repeated this mistake when responding to the international financial crisis in the fall of 1931.[xx]

Friedman argued that as a result the Federal Reserve reduced the money supply and the quantity in circulation declined throughout 1930.[xxi] This created a period of deflation as Richardson explains:

From the fall of 1930 through the winter of 1933, the money supply fell by nearly 30 percent. The declining supply of funds reduced average prices by an equivalent amount. This deflation increased debt burdens; distorted economic decision-making; reduced consumption; increased unemployment; and forced banks, firms, and individuals into bankruptcy. The deflation stemmed from the collapse of the banking system…[xxii]

The severe contraction of the money supply along with the bank panics made the Depression worse. The bank panics were the direct result of people who had lost confidence not only in the economy but were scared. The bank panics were symbolized by the famous “runs” on banks, which started in the Midwest and spread like wildfire as individuals pulled their savings out of banks.[xxiii]

As Secretary of Commerce, Hoover had been concerned about the “growing tide of speculation” that was occurring in the economy.[xxiv] Hoover argued that the Federal Reserve “had deliberately created credit inflation” during the 1920s.[xxv] President Calvin Coolidge even acknowledged “that the country was engaged in too much speculation.”[xxvi] Coolidge also agreed with Hoover that the Federal Reserve was trying to “check speculation” by raising interest rates, but the resulting economic collapse of international finance made the situation worse.[xxvii] Further, Coolidge argued, just as with Hoover, that “the causes of the Depression, with the exception of the early speculation, had their origin outside of the United States, where they were entirely beyond the control of our government.”[xxviii]

The question must be asked whether or not Hoover and Coolidge were correct that without the collapse of international finance the Great Depression would have resembled a severe correction as in past economic downturns. The actions of the Federal Reserve were in response to both internal and external economic forces, which resulted in a contraction of the money supply and deflation. The result was high unemployment, which reached as high as 25 percent, bank failures, business closures, and the further collapse of agriculture.

The evidence appears to be on the side of Hoover and Coolidge and Bernanke even acknowledges that the evidence of a “monetary contraction” is an important cause of the Depression.[xxix] In 2002, Bernanke who was a member of the Federal Reserve Board and speaking at an event honoring Milton Friedman, publicly acknowledged the Feds responsibility for causing the Depression.[xxx]

How the Great Depression was resolved is another issue of debate. A standard interpretation is that President Franklin D. Roosevelt’s New Deal resolved the banking crisis and saved capitalism, but it was World War II that finally ended the Depression. Economist Christina Romer credits monetary policy with easing the economy out of Depression.[xxxi]

“The very rapid growth of the money supply beginning in 1933 appears to have lowered real interest rates and stimulated investment spending…”[xxxii] Romer argues that the expansion of the money supply complements Friedman’s theories.[xxxiii] In addition, Romer makes the Keynesian argument that “aggregate-demand stimulus was the main source of the recovery from the Great Depression.”[xxxiv]

The question whether Roosevelt’s pump priming economic stimulus spending worked cannot be fully addressed in this article, but economic historian Burton W. Folsom, Jr. argues that the administration was planning on a return of the Depression once the war had ended.[xxxv]Folsom credits the final victory over the Depression with the fiscal conservative policies that emerged during the mid-1940s when Republicans joined with Southern Democrats to block further New Deal policies.[xxxvi]

In the mid-term elections of 1946, the Republicans took control of Congress, which resulted in fiscal conservative agenda. Folsom noted that Congress “lifted most economic controls, cut tax rates, slashed federal spending, and trusted entrepreneurs to create the jobs needed for returning soldiers.”[xxxvii] These fiscal conservative policies “revived the economy, which grew much faster in 1946 and 1947 than government experts had forecast, and unemployment stabilized at 3.9 percent.”[xxxviii] President Roosevelt’s New Deal never stabilized unemployment and the economy even fell into a recession during 1937.

“The Great Depression was finally over,” stated Folsom.[xxxix] From this perspective the cure of the Depression was not federal government stimulus and war mobilization, but rather a return to fiscal conservatism. Roosevelt’s Secretary of the Treasury Henry Morgenthau even admitted this when he stated:

We have tried spending money. We are spending more than we have ever spent before and it does not work. And I have just one interest, and if I am wrong…somebody else can have my job. I want to see this country prosperous. I want to see people get a job. I want to see people get enough to eat. We have never made good on our promises….I say after eight years of this Administration we have just as much unemployment as when we started….And an enormous debt to boot![xl]

Source: Old Reliable! American cartoon, 1938, by Clifford Berryman, Library of Congress

This brings up another question of debate. Monetary policy and the collapse of international finance may have caused the Great Depression, but would the outcome have been different if the federal government followed a non-interventionist approach? This was the case with the depression of 1920-1921 and previous economic downturns.

Benjamin M. Anderson, an economist and who also served as the economist for Chase Manhattan Bank, argued in Economics and the Public Welfare: A Financial and Economic History of the United States, 1914-1916, that the real blame for making the Depression “great” was the effort of “the United States [government] to play God.”[xli] Anderson was not just critical of the Federal Reserve, but also the policy interventions by the federal government, which directly interfered with markets.[xlii] Anderson even goes as far to argue that the New Deal actually began in 1924 during the administration of President Coolidge and continued with the Hoover and Roosevelt administrations.[xliii] Anderson’s view is highly critical of both the Republican administrations of the 1920s and Roosevelt’s New Deal and his view is closely aligned with libertarian and Austrian schools of economic thought.

The debate over the Great Depression will continue, but President Hoover’s argument that the combination of monetary policy and the collapse of international finance is accurate. The Federal Reserve, in responding to both internal and external economic forces, made the Depression worse, and its longevity was due to a large degree in the failed interventionist polices of Roosevelt’s New Deal.

[i]Ben S. Bernanke, “The Macroeconomics of the Great Depression: A Comparative Approach.” Journal of Money, Credit and Banking 27, no. 1 (1995): 1–28.

[ii]Herbert Hoover, The Memoirs of Herbert Hoover: The Great Depression, 1929-1941, New York: The MacMillan Company, 1952, v.

[iii]Ibid., vi.

[iv]Ibid.

[v]Michael Lind, Land of Promise: An Economic History of the United States, New York: Harper, 2012, 267.

[vi]Charles R. Morris, A Rable of Dead Money: The Great Crash and the Global Depression: 1929-1939, New York: Public Affairs, 2017, xv.

[vii]Ibid.

[viii]Ibid.

[ix]Hoover, vi.

[x]Hans F. Sennholz, “The Great Depression,” The Foundation for Economic Education, October 1, 1969, <https://fee.org/articles/the-great-depression/> (accessed on April 16, 2024).

[xi]Ibid.

[xii]Hoover, vi.

[xiii]Ibid.

[xiv]Lind., 272.

[xv]John Steele Gordon, An Empire of Wealth: The Epic History of American Economic Power, New York: Harper Collins Publishers, 2004, 323,

[xvi]Ibid., 323-324.

[xvii]Hoover, vi.

[xviii]Ibid.

[xix]Milton Friedman and Rose Friedman, Free to Choose: A Personal Statement, New York: Harcourt Brace & Company, 1980, 79-81.

[xx]Gary Richardson, “The Great Depression, 1929-1941,” Federal Reserve History, Federal Reserve Bank of St. Louis, < https://www.federalreservehistory.org/essays/great-depression> (accessed on April 16, 2024).

[xxi]Friedman, 79.

[xxii]Richardson.

[xxiii]Gordon, 330.

[xxiv]Hoover, 5.

[xxv]Ibid., 6.

[xxvi]Calvin Coolidge, “The Republican Case: Reprinted by Special Permission of the Saturday Evening Post,” Republican National Committee, 1932.

[xxvii]Ibid.

[xxviii]Ibid.

[xxix]Bernanke, 25.

[xxx]Richardson.

[xxxi]Christina D. Romer, “What Ended the Great Depression?” The Journal of Economic History 52, no. 4 (1992): 757–84.

[xxxii]Ibid., 781.

[xxxiii]Ibid., 782.

[xxxiv]Ibid., 783.

[xxxv]Burton W. Folsom, Jr., and Anita Folsom, FDR Goes to War: How Expanded Executive Power, Spiraling National Debt, and Restricted Civil Liberties Shaped Wartime America, New York: Threshold Editions, 2011, 280-281.

[xxxvi]Ibid., 310-311.

[xxxvii]Ibid., 311.

[xxxviii]Ibid.

[xxxix]Ibid.

[xl]Henry Morgenthau, Jr. quoted in Burton F. Folsom Jr., New Deal or Raw Deal: How FDR’s Economic Legacy Damaged America, New York: Threshold Editions, 2008.

[xli]Benjamin M. Anderson, Economics and the Public Welfare: A Financial and Economic History of the United States, 1914-1946, Indianapolis, Indiana: Liberty Fund, 1979, 483.

[xlii]Ibid.

[xliii]Ibid., 127.

Bibliography

Anderson, Benjamin A. Economics and the Public Welfare: A Financial and Economic History of the United States, 1914-1946. Indianapolis, Indiana: Liberty Fund, 1979.

Bernanke, Ben S. “The Macroeconomics of the Great Depression: A Comparative Approach.” Journal of Money, Credit and Banking 27, no. 1 (1995): 1–28.

Coolidge, Calvin. “The Republican Case: Reprinted by Special Permission of the Saturday Evening Post.” Republican National Committee, 1932.

Folsom, Burton W. Jr., and Anita Folsom. FDR Goes to War: How Expanded Executive Power, Spiraling National Debt, and Restricted Civil Liberties Shaped Wartime America. New York: Threshold Editions, 2011.

Folsom, Burton W. Jr. New Deal or Raw Deal: How FDR’s Economic Legacy Damaged America. New York: Threshold Editions, 2008.

Friedman, Milton and Rose Friedman. Free to Choose: A Personal Statement. New York: Harcourt Brace & Company, 1980.

Gordon, John Steele. An Empire of Wealth: The Epic History of American Economic Power. New York: Harper Collins Publishers, 2004.

Hoover, Herbert. The Memoirs of Herbert Hoover: The Great Depression, 1929-1941. New York: The MacMillan Company, 1952.

Lind, Michael. Land of Promise: An Economic History of the United States. New York: Harper, 2012.

Morris, Charles R. A Rable of Dead Money: The Great Crash and the Global Depression: 1929-1939. New York: Public Affairs, 2017.

Richardson, Gary. “The Great Depression, 1929-1941.” Federal Reserve History. Federal Reserve Bank of St. Louis. < https://www.federalreservehistory.org/essays/great-depression> (accessed on April 16, 2024).

Romer, Christina A. “What Ended the Great Depression?” The Journal of Economic History 52, no. 4 (1992): 757–84.

Sennholz, Hans F. “The Great Depression.” The Foundation for Economic Education. October 1, 1969. <https://fee.org/articles/the-great-depression/> (accessed on April 16, 2024).

Print a PDF

Print a PDF