The Iowa Legislature should seize the opportunity to speed up income tax cuts and lead the state toward a full income tax repeal.

The last few years have been historic for state-based tax reform across the country. The Tax Foundation reports that 43 states passed some form of tax reform in 2021 and 2022. In 2022, Iowa led the nation in what Forbes contributor Patrick Gleason described as a “flat tax revolution.” Gleason, who also serves as vice president of state affairs at Americans for Tax Reform, suggests the United States is in a “golden era of state tax relief.”

Source: Tax Foundation

Jonathan Williams, chief economist at the American Legislative Exchange Council (ALEC), describes 2023 as “another banner year for state tax cuts.” Many states are building upon previous tax-rate reductions or accelerating previously enacted tax cuts. Furthermore, Williams argues that “states are focusing on the right kind of taxes to cut, income and capital-based taxes.” Taxes on income are the most harmful because they punish economic growth and productivity; they also reduce incentive for individuals to work or to start or expand businesses.

With more states lowering income tax rates, Iowa must not become complacent. During the next legislative session, the Iowa Legislature should seize the opportunity to lower tax rates, placing the income tax on a path toward full repeal. States are increasingly in competition with each other for both jobs and people. A mass exodus is occurring as people flee high-tax states to states with better tax climates. This movement has been amplified as individuals become better able to take advantage of remote work and businesses and entrepreneurs can more easily shop around for the best local conditions in which to expand or start new businesses.

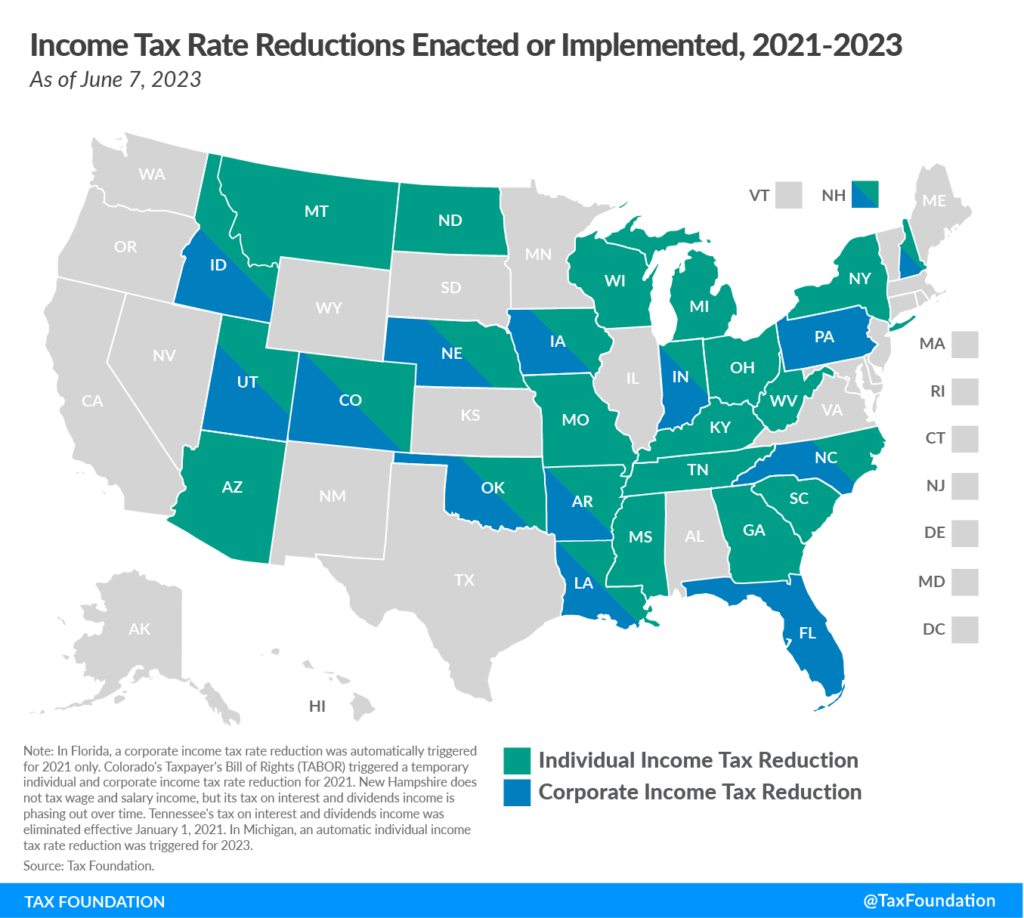

A Banner Year for Tax Relief

While state tax reform is mostly occurring in Republican “red” states, even some Democrat “blue” states are considering lowering rates. Connecticut, for example, is a progressive state that has lowered its income tax on the two lowest marginal rates. Progressive Wisconsin is also considering income-tax reforms, although the possibility an agreement can be reached remains uncertain. One reason Republican states have been reducing tax rates is their principled emphasis on competitive federalism, leading to a healthy contest not only in pro-growth tax policy, but also in other policy areas, such as school choice. This competitive “red state” federalism is driving pro-growth tax policy across numerous states.

Iowa’s neighbor, Nebraska, has already enacted income tax reform this year. According to the Tax Foundation, Nebraska will reduce its top individual income tax rate from 6.64 percent to 3.99 percent by 2027. The state’s top corporate tax rate of 7.25 percent will be reduced to 3.99 percent over the same period. By 2027, Nebraska’s corporate tax rate will be much lower than Iowa’s, which is set to phase down in line with a revenue trigger until it reaches a flat 5.5 percent.

North Dakota also enacted tax reform to lower its individual income tax. The state’s top rate is currently 2.9 percent, with five rate brackets, which will be reduced to two brackets: a top rate of 2.5 percent and a lower rate of 1.9 percent. Montana, meanwhile, is accelerating its income tax reforms. The legislature passed a measure that will lower the income tax rate from its current 6.75 percent until it reaches 5.9 percent in 2024.

Kentucky, which has a flat income tax, enacted a tax reform law that will lower the 4.5 percent rate to 4.0 percent by 2024. Indiana, which has made considerable progress over the last several years in gradually lowering both individual and corporate income tax rates, passed legislation to lower its individual income tax more quickly than was already planned. The current rate of 3.15 percent will drop to 3.05 percent in 2024, and existing triggers will be removed until the rate reaches 2.9 percent by 2027.

Arkansas is building upon previous tax reform by further lowering both its individual and corporate tax rates. Currently the top individual income tax rate in the state is 4.9 percent, and the top corporate rate is 5.3 percent. Under its updated tax law, the top individual rate will be lowered to 4.7 percent, and the top corporate rate to 5.1 percent. In West Virginia, Governor Jim Justice signed an extensive income tax reform measure. After several years of trying to implement income tax reform, the state succeeded in enacting the largest tax cut in its history. The reform reduces rates in all five income tax rate brackets, with the top rate dropping from 6.5 percent to 5.12 percent.

Other states are considering income tax reforms, such as Ohio and North Carolina. The Ohio Senate has proposed replacing its current four-bracket income tax and replacing it with two brackets. The proposal would lower the top rate from 3.99 percent to 3.5 percent and create one lower bracket at 2.75 percent. North Carolina, which was an early leader in state tax reform, is looking at continued lowering of rates. Currently, North Carolina’s individual income tax rate is 4.75 percent, and its House has proposed an accelerated reduction to 4.5 percent by 2024. The state’s Senate has a more aggressive proposal that would lower the rate to 2.49 percent by 2027. North Carolina has already passed legislation that will phase out its corporate tax by 2030.

What Can Iowa Do Next?

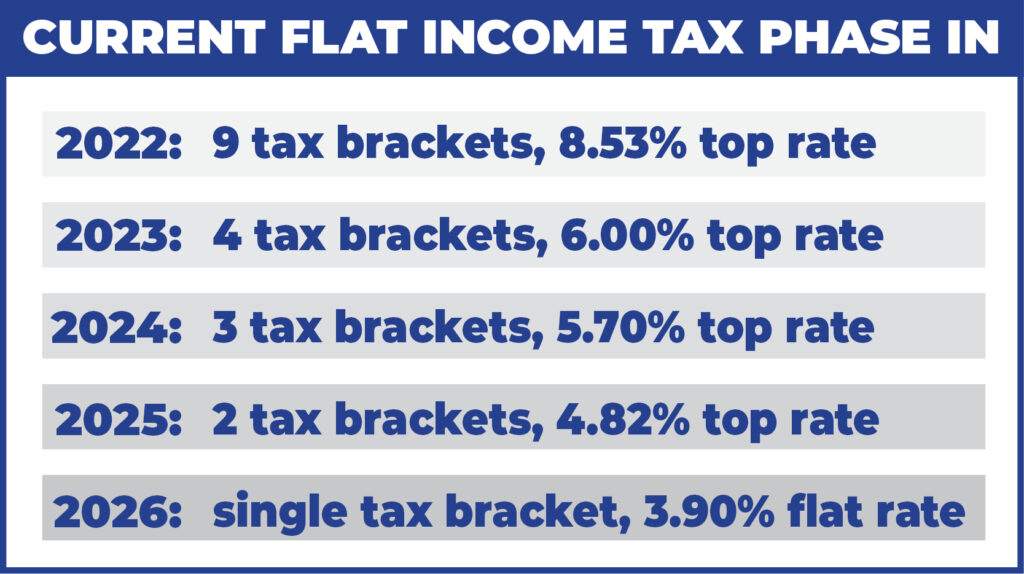

At this time, Iowa is still a national leader. Governor Kim Reynolds and the legislature have made tax reform and making Iowa’s tax code competitive a priority. Iowa’s historic tax reform, which will replace the nine-bracket progressive income tax with a flat 3.9 percent rate is the most transformational. Nevertheless, Governor Reynolds has stated that changes to the income tax are far from over.

As was true in North Carolina, Iowa has been able to pass pro-growth tax policies on the strength of conservative budgeting. By controlling and limiting spending, Governor Reynolds and the legislature have opened the way for pro-growth policies. Consequently, Iowa’s fiscal house rests on a firm foundation. The state is running budget surpluses, and its reserve accounts are full to their statutory maximums. The government estimates that Iowa will have a $2 billion budget surplus in fiscal year 2024.

Further income tax reform is therefore likely to be a priority for the 2024 legislative session. Even with the national economic uncertainty caused by high inflation and the reckless fiscal policies of the federal government, Iowa is still in a solid position to build upon the 2022 tax reform and lower its flat tax to match Arizona’s 2.5 percent rate.

This past session, the Iowa Senate introduced a comprehensive income tax reform measure that would have placed the income tax on a path toward elimination. Senator Dan Dawson, who chairs the Ways and Means Committee, proposed to accelerate the phase in of the 2021 income tax cuts, and further cut the 3.9 percent flat tax rate to 2.5 percent in 2028.

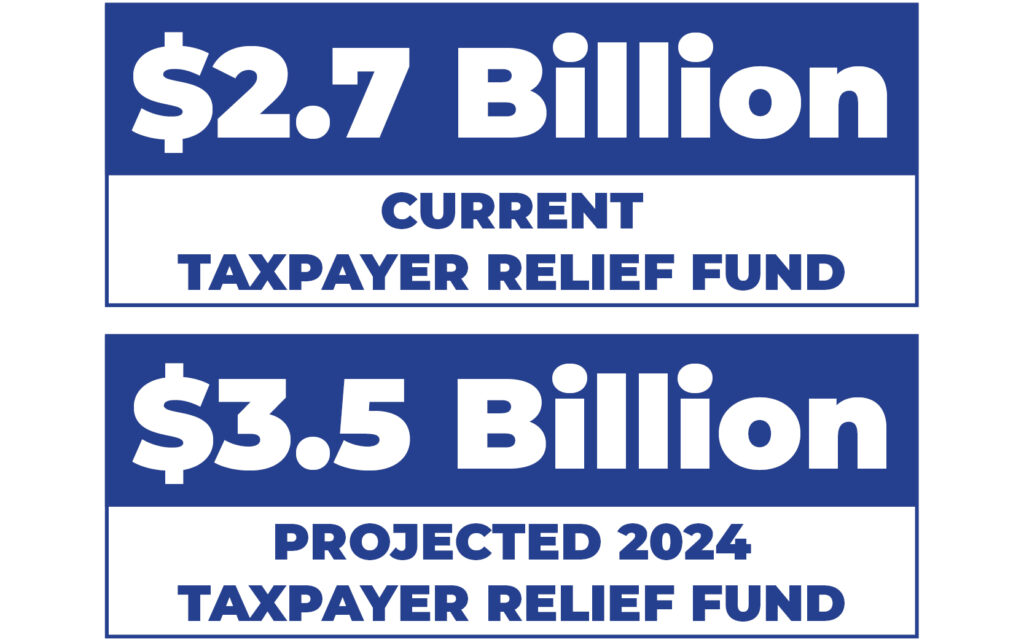

Once the 2.5 percent flat rate is implemented for the individual income tax, the next stage would be to phase it down until completely eliminated. Senator Dawson’s plan does this by utilizing Iowa’s growing Taxpayer Relief Fund. The fund sets aside the overpayment of state taxes for the purpose of providing Iowans with future income tax relief. Currently, the Taxpayer Relief Fund has a $2.7 billion balance, which is expected to increase in fiscal year 2024 to $3.5 billion. Estimates find that, under the Senate proposal, the income tax could be eliminated as early as 2030.

Iowa is in a unique situation for future income tax relief because of the Taxpayer Relief Fund. Created in 2011, and originally named the Taxpayer Trust Fund, the original intent was to ensure that excess revenues would be collected and returned to taxpayers. The dollars in the Taxpayer Relief Fund represent an overcollection of income and sales taxes and therefore it is the responsibility of the legislature to return the taxpayer’s money back to them through income tax reductions.

With such massive balances that continue to grow the Taxpayer Relief Fund will provide the opportunity for policymakers to return this money back to the taxpayer. Nevertheless, policymakers must avoid the temptation of raiding the Taxpayer Relief Fund for additional spending, local government aid, or even shifting dollars to the General Fund in order to provide property tax relief.

Accelerating the 2022 tax rate reductions and going beyond the 3.9 percent flat rate or even placing the income tax on a path of elimination would benefit all Iowa taxpayers. Next year Iowa has the opportunity to continue to be the leader in this “golden era of state tax relief.”

Print a PDF

Print a PDF