This article was published in the Washington Examiner and Dubuque Telegraph Herald.

Iowa should use the significant progress made in the nation lowering income tax rates as a source of momentum for further improvements.

The last few years have been historic for state-based income tax reforms, and Iowa has become a national leader in this revolution as a result of its transformational 2022 tax reform measure. The 2022 tax reform was not only the largest reform in state history, but it is also the most extensive state-based tax reform in the nation.

Patrick Gleason, the vice president of state affairs at Americans for Tax Reform, has described recent developments as a “golden era of state tax relief.” Jared Walczak, vice president of state projects at the Tax Foundation, agrees, saying, “The past three years have seen the largest wave of state-tax cuts in the modern era, certainly since income taxes were created over a century ago at the state level.” The Tax Foundation reports that 43 states passed some form of tax reform in 2021 or 2022. This year, several more states enacted income tax reform measures that reduced rates.

Iowa’s leadership in the state “flat tax revolution” has been a long time coming. The Iowa legislature levied its first income and sales taxes in 1934, ostensibly to provide property tax relief. At that time, the progressive income tax had five brackets, with the highest being five percent. The income tax soon began increasing until it reached a top rate of 13 percent with 13 tax brackets in 1975. Legislation in 1987 reduced the number of brackets to nine, with a top rate of 9.98 percent. However, Iowa’s first substantial tax reform measure came in 1998, with a 10 percent across-the-board rate cut, keeping all nine brackets.

Iowa’s corporate tax has a similar story. The state first levied the tax in 1934, at a flat two percent. Not until 1967 did the progressive tax structure find its way to this tax, with three brackets and a top rate of 8 percent. This structure increased to four brackets in 1981, with a top rate of 12 percent — the highest in the nation.

Throughout these changes, federal deductibility and numerous tax credits often “softened” the burden of Iowa’s high income tax rates. The IRS allowed a reduced federal tax burden to subsidize state taxes, and for decades, policymakers in Iowa turned to tax credits to provide additional tax relief and, often, to implement other policies by means of the tax code.

After Congress passed the Tax Cuts and Jobs Act, which among other things reduced the amount of state and local taxes filers could deduct, tax reform became a priority for Governor Kim Reynolds and the Republican-controlled legislature. In 2018, the Iowa Legislature passed, and Governor Reynolds signed into law, what was then the largest income tax cut in state history. The reform not only lowered individual and corporate rates but also made comprehensive changes to modernize and reform other aspects of Iowa’s tax code.

This reform maintained the progressive income tax but reduced the brackets from nine to four, with a top rate of 6.5 percent, taking effect in 2023. The corporate tax also remained a progressive tax with four brackets, but rates were lowered, topping out at 9.8 percent.

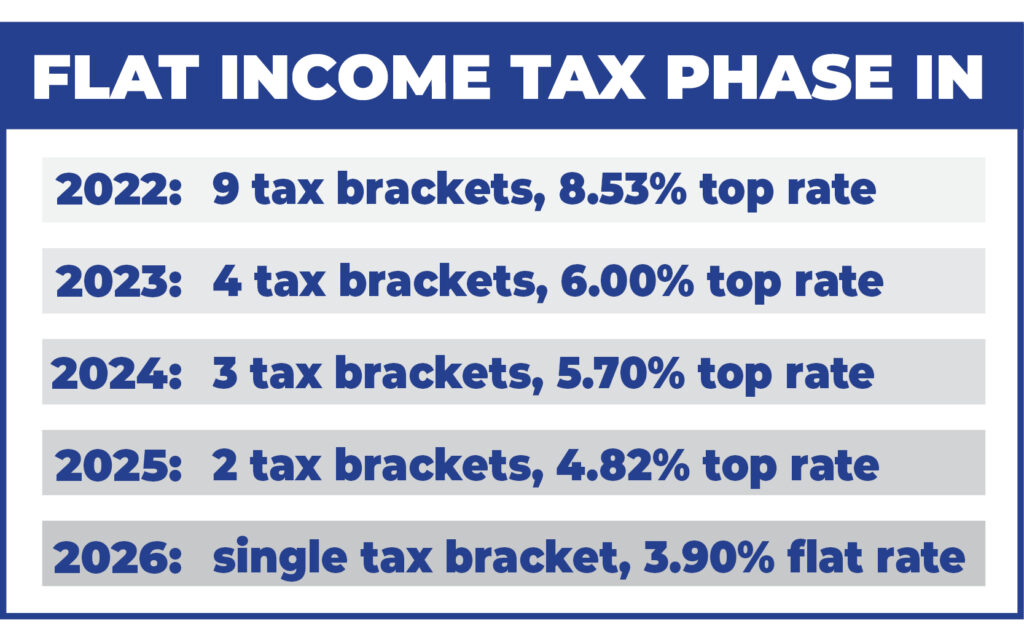

Subsequently, the legislature surpassed the 2018 tax reform measure in 2022. This follow-up reform also was comprehensive and will completely phase out the current progressive nine-bracket income tax system, replacing it with a flat 3.9 percent rate by 2026, as follows:

The corporate tax rate will also be lowered until it reaches a flat 5.5 percent. In this case, reductions are tied to a state-revenue trigger, which has already resulted in a drop from 9.8 percent to 8.4 percent. According to current projections, the 5.5 percent flat rate will also be achieved by 2026.

With the 2022 legislation, Iowa implemented a change in tax policy Americans for Tax Reform’s Gleason named as “the most significant” in the country, putting Iowa on the same path as North Carolina, the gold standard in state tax reform for years. North Carolina started a period of historic tax reforms in 2013 that continues to this day. Beginning with some of the highest tax rates in its region (although not as high as Iowa’s), North Carolina’s progressive income tax imposed three brackets with a top rate of 7.75 percent.

To initiate its reform, the state replaced this structure with a flat tax of 5.8 percent, which has since been lowered to 5.25 percent. North Carolina also lowered its corporate tax rate from 6.9 percent to 2.5 percent and will completely phase it out by 2029. The improvement has been dramatic. In 2014, North Carolina ranked 31 out of 50 on the Tax Foundation’s State Business Tax Climate Index. It is now in the top 10 (10th in the 2023 index).

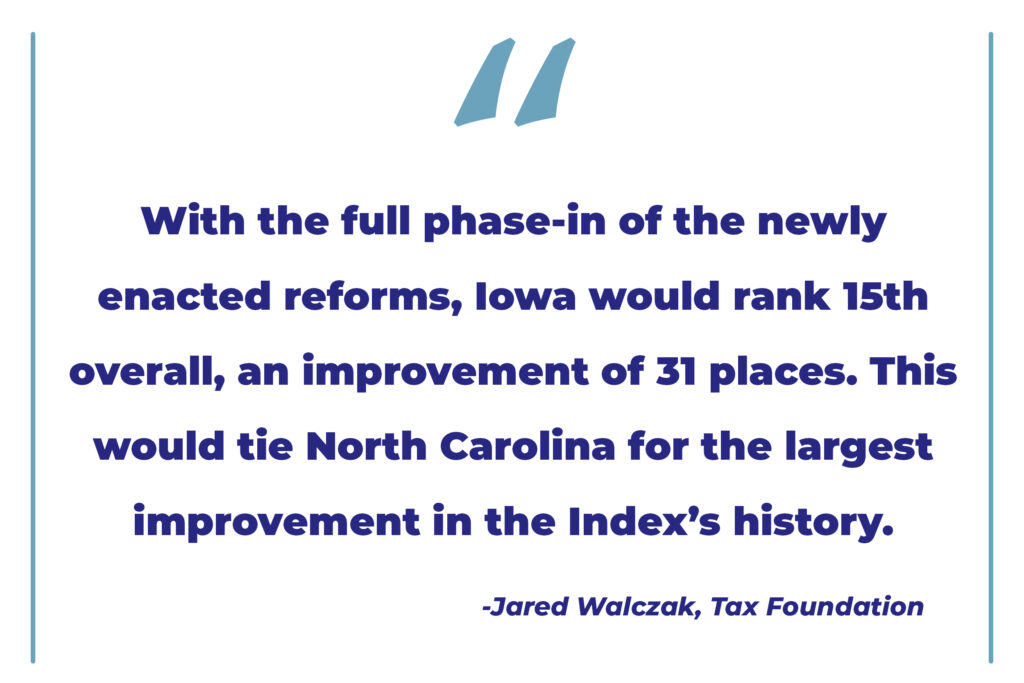

Before its reform, Iowa’s situation was even worse in the Tax Foundation’s eyes. In fact, our state was often in the top 10 states for the worst tax climate. In 2014, the index ranked Iowa 45, which has moved up to 38 in the current rankings. Once Iowa’s 2022 reforms are fully implemented, the Tax Foundation expects even greater improvement. “With the full phase-in of the newly enacted reforms, Iowa would rank 15th overall, an improvement of 31 places. This would tie North Carolina for the largest improvement in the Index’s history,” notes Jared Walczak.

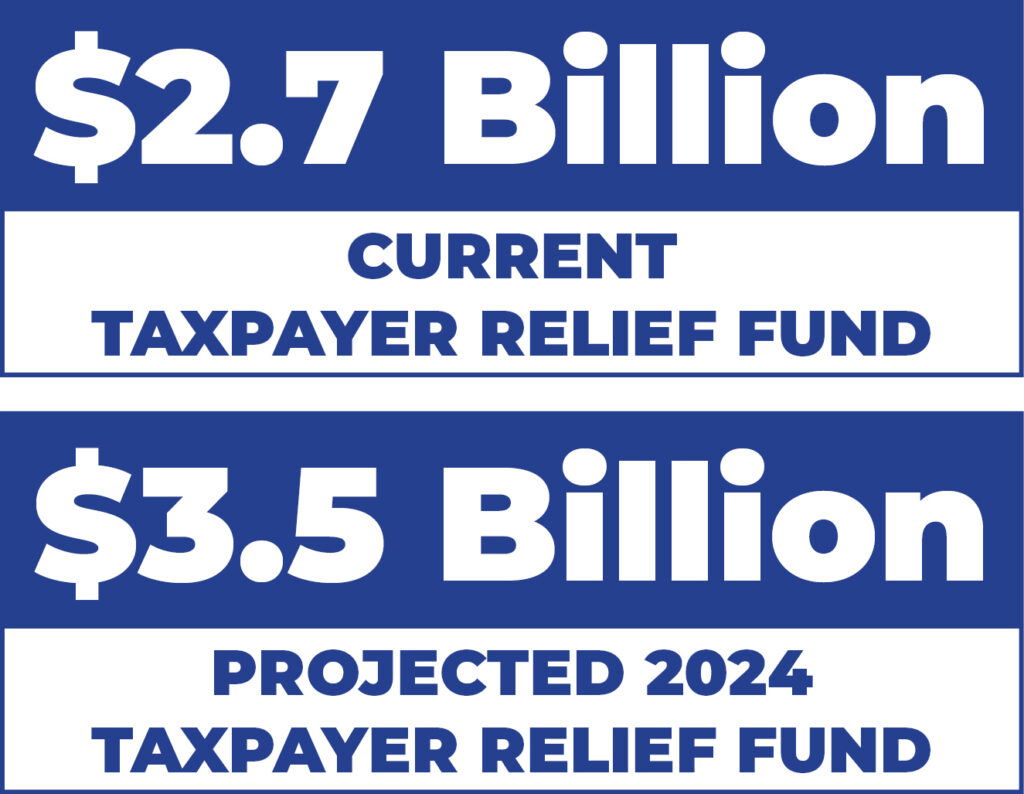

The formula for Iowa’s and North Carolina’s success involves two central policy principles: prudent budgeting and gradually lower rates. A sound tax policy must begin with limits on spending. Governor Reynolds and the legislature have made conservative budgeting a cornerstone of their policy agenda. Iowa is anticipating a $1.7 billion surplus for fiscal year 2023, building on a $1.9 billion surplus in fiscal year 2022. The state forecasts an estimated $2 billion surplus in fiscal year 2024. In addition, Iowa’s reserve funds are fully funded at their maximum limit and are projected to increase in future fiscal years and the Taxpayer Relief Fund is estimated to grow its balance to $3.5 billion in 2024.

With this fiscal foundation, Governor Reynolds told a Cato Institute audience that Iowa is far from finished with tax reform, saying her goal is to eliminate the income tax altogether. In keeping with this goal, Senator Dan Dawson, Chair of Ways & Means Committee, introduced a bill that would not only speed up rate reductions, but create an even lower flat tax that places the income tax on a path toward elimination. Senator Dawson’s plan would lower the individual income tax to a flat 4 percent in 2025, falling to 3.9 percent in 2026. By 2027, the rate would hit 2.95 percent, and by 2028, it would be lowered to 2.5 percent. The proposal would also continue corporate tax rate reductions, with the goal of phasing down the rate to a flat 4.75 percent, instead of the current target of 5.5 percent.

Meanwhile, the individual income tax would shrink from the 2.5 percent rate to zero utilizing the Taxpayer Relief Fund, which Dawson proposes to rename the Individual Income Tax Elimination Fund. Originally intended for the purpose of providing Iowans with income-tax relief, the Taxpayer Relief Fund has a $2.7 billion balance, which is expected to increase in fiscal year 2024 to $3.5 billion. Under Senator Dawson’s plan, the income tax could be eliminated by 2030.

Apart from a priority for intelligent, fair policy, motivation for continued reform comes from the fact states are in economic competition for both businesses and people. The rise of remote work has created incentive for individuals to relocate to states that have lower tax burdens. South Dakota, for example, is running television ads enticing people to relocate for new opportunities in an environment with zero state income tax. Arizona currently has the lowest flat tax, at 2.5 percent. North Dakota, while not a flat tax state, will also have a 2.5 percent rate. This year, Nebraska enacted tax reform that lowers their income tax to 3.99 percent, which will only be slightly higher than Iowa. Both Ohio and North Carolina are on a path to lower their income tax rate to 3.99 percent. Indiana is phasing down their flat income tax until it reaches 2.9 percent in 2029.

Iowa has already made the most significant progress in the nation lowering its income tax rates for a pro-growth and taxpayer-friendly tax code. Rather than thinking the job is done, policymakers should think of these results as a source of momentum for further improvements.

Print a PDF

Print a PDF