One of the foundational arguments for creating a Local Option Sales Tax was to offset the property tax burden. However, the property tax reduction has not come to fruition for many Iowa communities, leaving citizens with a higher sales tax burden and an increasing property tax burden, too.

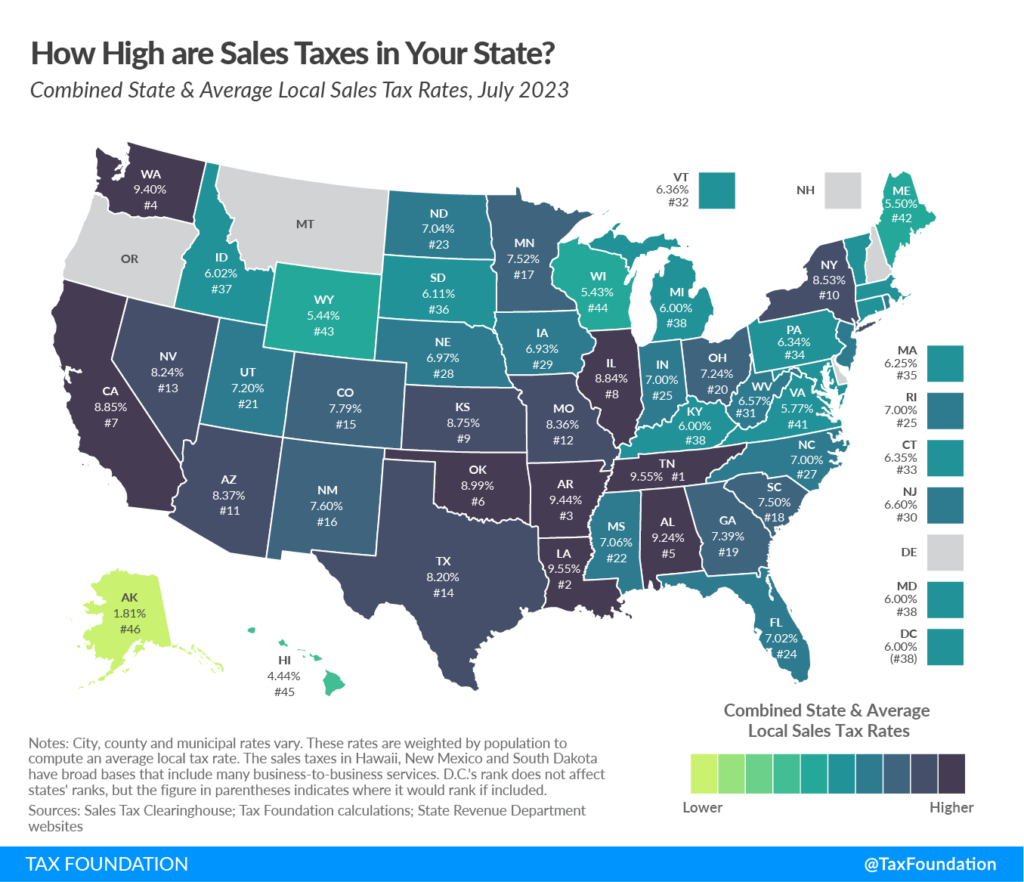

After the property tax, local sales taxes are the most-important source of tax revenue for local governments nationwide. Forty-five states and the District of Columbia collect statewide sales taxes, with local sales taxes collected in 38 states, one of which is Iowa.

While Iowa’s state sales tax sits at 6%, cities and counties have the option to impose an additional 1% local sales tax, referred to as the Local Option Sales Tax (LOST). If a county and a city in the same jurisdiction enact this sales tax through a vote of the people, the local rate is set at 1%, for a total sales tax rate of 7% in that area. Importantly, cities and counties don’t each get to levy the tax; in some cases, cities or unincorporated areas might levy the tax while others in the same county do not.

When measured statewide, the average sales tax is 6.93% because a LOST has been adopted in most, but not all, cities and unincorporated areas in Iowa, giving the state the 29th highest combined state and local sales tax rate in the nation. As with the statewide sales tax, a LOST is imposed on the final sale of most goods and services, with food, prescription drugs, professional services, and other statewide exemptions applying to the local portion, as well.

What Is a Sales Tax?

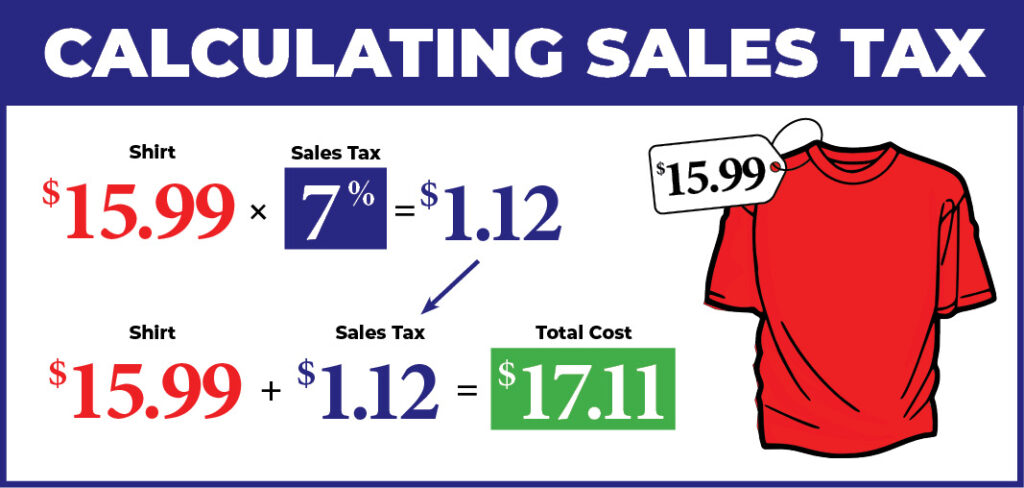

A sales tax is an ad valorem tax — that is, a percent of the price of the item added to the final purchase amount upon purchase. For example, if you buy a shirt for $15.99 with a sales tax rate of 7 percent, your total bill will be $17.11 because of the tax.

In economic terms, a sales tax is a consumption tax because it is levied when someone “consumes” a product. Across the country, sales taxes typically exempt certain items. Each state exempts different goods and services, and each has a slightly different structure. As noted above, five states choose not to levy a sales tax at all, while others rely on the sales tax as their main source of state tax revenue. Some states have a significant number of exemptions, whereas others have very few.

History of Iowa’s Local Option Sales Tax

In 1985, Iowa’s state legislature passed a law (SF395) allowing local governments to impose a LOST on top of the state sales tax to raise additional revenue for specific projects and needs within their communities. The new legislation allowed cities and counties to impose a 1% LOST after a successful vote of the people. The tax could be imposed in a city, county, or unincorporated portion of a county, and all revenue collected would be distributed according to a formula (provided below). Local governments could use the funds for any lawful purpose, including, among others, property tax relief and bond collateral.

During its 1998 session (with bill HF 2282), the legislature approved an additional 1% local option tax for school infrastructure. The passage of the School Infrastructure Local Option (SILO) Sales Tax in addition to the 1985 LOST resulted in a total tax rate of 7% in some jurisdictions (5% state + 1% LOST + 1% SILO). In 2008, the state increased its sales tax rate from 5% to 6%, earmarking the additional percentage point to school infrastructure through the Secure and Advanced Vision for Education (SAVE) fund and repealed the SILO, maintaining the maximum sales tax rate of 7%.

Since 2008, the number of cities with a LOST has grown to a total of 923, and total revenue was over $600 million in fiscal year 2022 (FY22). That leaves only 17 cities that do not have a LOST.

Proposed changes during the 2023 legislative session (in bill SF 550) would have eliminated LOST in exchange for increasing the state sales tax rate from 6 to 7%. A Natural Resources and Outdoor Recreation Trust Fund portion of the sales tax would have been implemented along with changed distributions to all cities and counties. The bill never advanced from committee.

Policy Considerations Associated with Local Option Sales Taxes

Local-option sales taxes raise many policy issues — some benefits, like promoting local autonomy and administrative efficiency, and some drawbacks, like reduced state flexibility.

Local Autonomy

LOST is a direct source of revenue that helps local governments maintain autonomy over their fiscal affairs, even though local control over the tax is limited. In Iowa, the rate and base are established by the legislature, and local governments cannot modify it. The state collects the tax and returns a portion of it to the localities that have levied it, making it essentially an intergovernmental transfer of revenue. Even with this limited control, the tax serves as a continuous source of revenue that can be spent broadly and is not dependent upon yearly appropriations by the state legislature.

Administrative Efficiency

Local governments have few administrative responsibilities with a LOST and incur almost no costs to enact it. For their part, residents incur no direct compliance cost, and the burden is primarily on the vendor to collect and remit the tax to the state. The state then returns the local portion of the tax to the counties where the sales were made. Additional duties for auditing and enforcing collections also fall onto the state, again relieving municipalities of this task. While additional complexity arises for vendors with locations in multiple areas, the additional burden is not a huge concern in Iowa because almost all municipalities have chosen to levy the tax.

Interjurisdiction Competition

On the negative side, LOSTs are an inefficient method of collecting tax in an environment of competitive interlocal government systems. Because the tax increases the cost of consumption to consumers, citizens have incentive to shop in cities and towns that offer lower overall tax burdens. For example, the city of Ankeny does not impose a LOST. This means shoppers in the Des Moines metro area might choose to shop there to take advantage of the lower tax burden.

Incentives also change for local governments. Once the tax is in place, it often spurs competition for retail development. The more a community relies on the local sales tax, the more incentive officials have to encourage the building of retail shopping space to enhance revenue. Ironically, local governments’ competition to attract retail development can involve tax incentives, eroding any profit generated from the tax!

Regressivity

A regressive tax is one that falls disproportionately on lower-income individuals. Because the sales tax is levied on consumption, which includes necessities and regular activities, low-income individuals tend to find a higher percentage of their incomes subject to the tax. Naturally, this effect is greater in states with fewer exemptions for staples like food, medicine, and utilities. In an attempt to remedy the repressiveness of Iowa’s sales tax, state lawmakers have exempted necessities like prescription medicine and groceries. However, the LOST percentage does apply to utility payments.

Reduced State Flexibility

Another problem with LOST is its reduction of the state government’s flexibility with the state sales tax. When a local tax is added to a state rate, the overall tax rate climbs, as neither government has incentive to reduce the other’s burden on consumers. LOST also restricts the state’s ability to provide tax relief, because local governments become heavily dependent on the tax and lobby against any reduction or changes to the tax base.

Both North Carolina and Virginia, for example, ended their state sales taxes on groceries, but responding to the financial pressure on local governments, they did not remove groceries from the LOST base. In fact, some North Carolina cities want revenue so badly they are passing resolutions requesting authorization to impose more sales taxes on residents, pushing the rate in some jurisdictions to 7.5% in a state that only collects 4.75%.

Impact on Property Taxes

The growth of LOST jurisdictions can be seen as an attempt to shore up local budgets constrained by property tax limitations. One of the foundational arguments for creating a LOST in the 1980s was to offset the property tax burden paying for essential services. However, the property tax reduction has not come to fruition for many Iowa communities, which have experienced increasing overall spending, leaving citizens with a higher sales tax burden and an increasing property tax burden, too.

When implementing a LOST, Iowa cities must adopt a Revenue Purpose Statement describing how the revenue will be used and include it with the ballot at the time of election. While property tax relief is an approved purpose for LOST, it is only one option and not required. The city of Solon used its LOST funds for a new fire department station; Swisher funded a street development project; and Waukee recently built the 66-acre Triumph Park with LOST money. While others, such as Mason City, Knoxville, and Harlan, have dedicated 50% of their LOST revenue to property tax relief, and Sioux City dedicated 60% to that purpose, the remainder went to new projects and spending, ultimately driving up overall budgets.

Questions

Answers to the following questions about Iowa’s LOST derive from the website of Iowa’s Department of Revenue, which addresses many other inquiries.

How Is the Tax Imposed on a Local Area?

In Iowa, a LOST must be put on the ballot and approved by a majority of voters in an election. The proposal for the tax may come directly from the citizens in the form of a petition presented to the county board of supervisors. Alternatively, governing bodies representing at least half of the population of the county may propose the tax. In the case of a city, a motion of the governing body will suffice.

The vote itself can be held during a general or special election and repealed in the same way after a full year in effect. The election may be countywide or only in specific cities or unincorporated areas, but the result only applies to those areas in which a majority votes in favor of the tax. So, potentially one town or unincorporated area in a county could have the tax and another not, depending upon the outcome of the election. The tax rate can be no more than 1 percent.

What Can the Revenue Be Used For?

The taxes collected can be used for a wide variety of purposes, including property tax relief. However, in certain qualified counties, at least 50 percent of the LOST revenue must be used for property tax relief if the local sales and services tax election was held on or after January 1, 2019.

Will a Jurisdiction Receive the Actual Amount of Tax Collected by Merchants in the Locality?

No. The LOST revenue collected within a county is placed in a special distribution fund. It is distributed on the basis of population and property tax levies based on the formula described in the next section.

How Does the Local Option Sales Tax Distribution Formula Work?

Each county's account is distributed in proportion to population (75 percent) and property tax levies (25 percent). The population factor is based on the most recent certified federal census; the property tax factor is the sum of property tax dollars levied by boards of supervisors or city councils for the three years from July 1, 1982, through June 30, 1985. The property tax data is compiled from city and county tax reports available in the State Department of Management. Only population and property tax levies of the jurisdiction imposing the tax are used in figuring percentages.

The actual distribution is computed as follows:

D = (0.75 x P x Z) + (0.25 x V x Z)

Where:

Examples of an actual distribution are available in 701 Iowa Administrative Code § 270.10.

How Long Does the Local Option Sales Tax Remain in Effect Once It Is Imposed?

If the ordinance contains a sunset provision, the tax remains in effect until that date. If there is no sunset provision, the tax stays in effect for an unlimited period until repealed in a subsequent election.

Print a PDF

Print a PDF