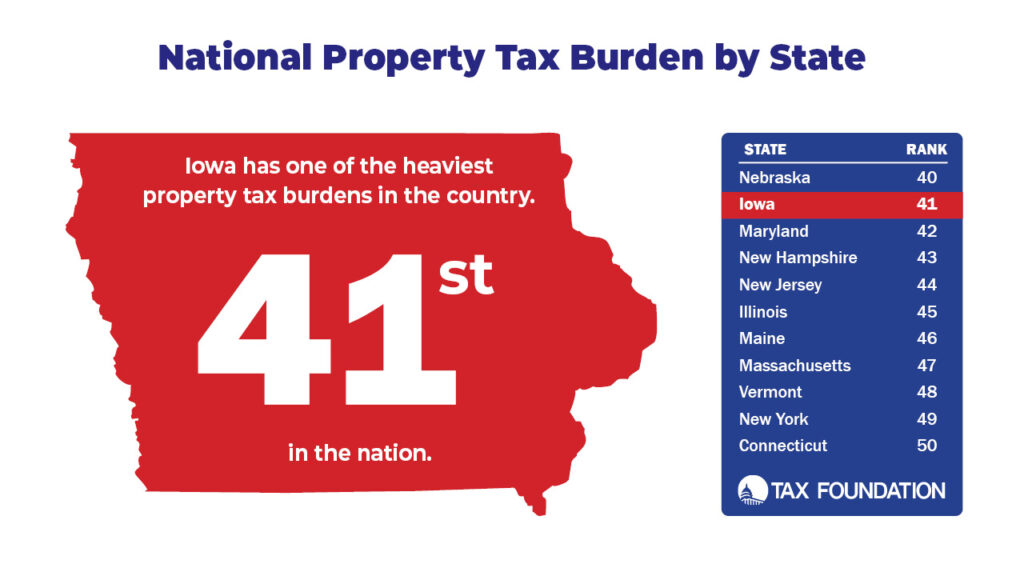

Iowa still ranks in the “Bottom 10” nationally when comparing property taxes.

The Tax Foundation recently released its annual 2024 State Business Tax Climate Index, which measures the tax competitiveness across the country. Iowa’s standing on the index has been improving every year, and thanks to continuing tax reforms, the 2024 results continued the trend. Last year, Iowa ranked 38th overall; the state now ranks 33rd. Once Iowa’s flat tax is completely phased in by 2026 it is estimated that Iowa will be ranked 15th overall.

But considering Iowa’s ranking in each tax sub-category of Tax Foundation’s provides a sense of where we’ve done well and where we need a sharper focus. And the property tax category, where Iowa is still a “bottom 10” state, stands out. Although the legislature recently passed a comprehensive property tax reform measure that will begin addressing the high property tax burden, more work is needed in this area.

Since 2000, total property taxes collected in Iowa have increased 119 percent — more than the increase in population, inflation, and the cost-of-living adjustment for Social Security. Iowans across the political divide, and those in both rural and urban communities, are demanding property tax relief and challenging local government officials’ excuses for not lowering property tax bills.

To address the main cause of high property taxes, local government spending, the legislature could consider implementing spending limitations. When implemented wisely, spending limits do not prevent local governments from fulfilling their responsibilities; they simply require officials to earn the people’s support and make government, and its spending, more accountable.

Surprisingly, New York may be the state Iowa should emulate for property tax limitations. While not generally considered a fiscally-conservative state, residents of most New York communities benefit from one of the best pro-taxpayer laws in the country. The Empire State has a property tax cap in place, which limits the annual growth of property taxes levied by local governments and school districts to 2% or the rate of inflation, whichever is less. This delivers multiple benefits:

1. Property Tax Relief: The primary benefit is preventing excessive tax increases, providing relief to the bottom line of homeowners and businesses.

2. Fiscal Discipline: The spending limit encourages local governments to be fiscally responsible and to prioritize spending within their means. It discourages reckless spending and forces local officials to carefully consider budget allocations.

3. Predictability: Property owners can more accurately predict their property tax bills. This predictability can be particularly beneficial for fixed-income residents and businesses.

4. Economic Growth: By limiting property tax increases, the spending cap can create a more favorable environment for economic growth and business development. Lower property taxes help attract new businesses and encourage investment.

Print a PDF

Print a PDF