Voters should pay close attention to why a district wants a Revenue Purpose Statement (RPS) and what it intends to do with the proceeds.

Details

A Revenue Purpose Statement (RPS) is a ballot measure describing how a school district will spend sales tax funds the State of Iowa has dedicated to public schools through a program called Secure an Advanced Vision for Education (SAVE). State law mandates that all SAVE money must be used to pay for local property tax relief or school infrastructure needs. If a district wants to utilize its SAVE funds on infrastructure projects by spending that money or bonding against it, officials must ask voters to approve an RPS allowing them to forgo property tax relief.

Importance

Simply put, if the voters of your district do not approve of a Revenue Purpose Statement (RPS), your property taxes will be lower. If they approve an RPS, your school district can spend more money and keep taxes higher. All school districts receive the corresponding funds from the state regardless of RPS status; the question is where the money goes.

How Property Taxes Are Lowered

If a school district does not have an RPS, the SAVE revenue generated from the sales tax must be used to reduce specific local property tax levies. The only exception is if voters previously approved an RPS and the district used it for revenue bonding, then that debt must be paid off before SAVE revenue can be directed towards tax relief. The district must apply the money in the following order:

To see how much your district is spending in property taxes, go to https://itrlocal.org/.

RPS on the Ballot

Every March and September a handful of districts submit RPSs to voters. Voters should pay attention to why a district wants an RPS and what it intends to do with the proceeds.

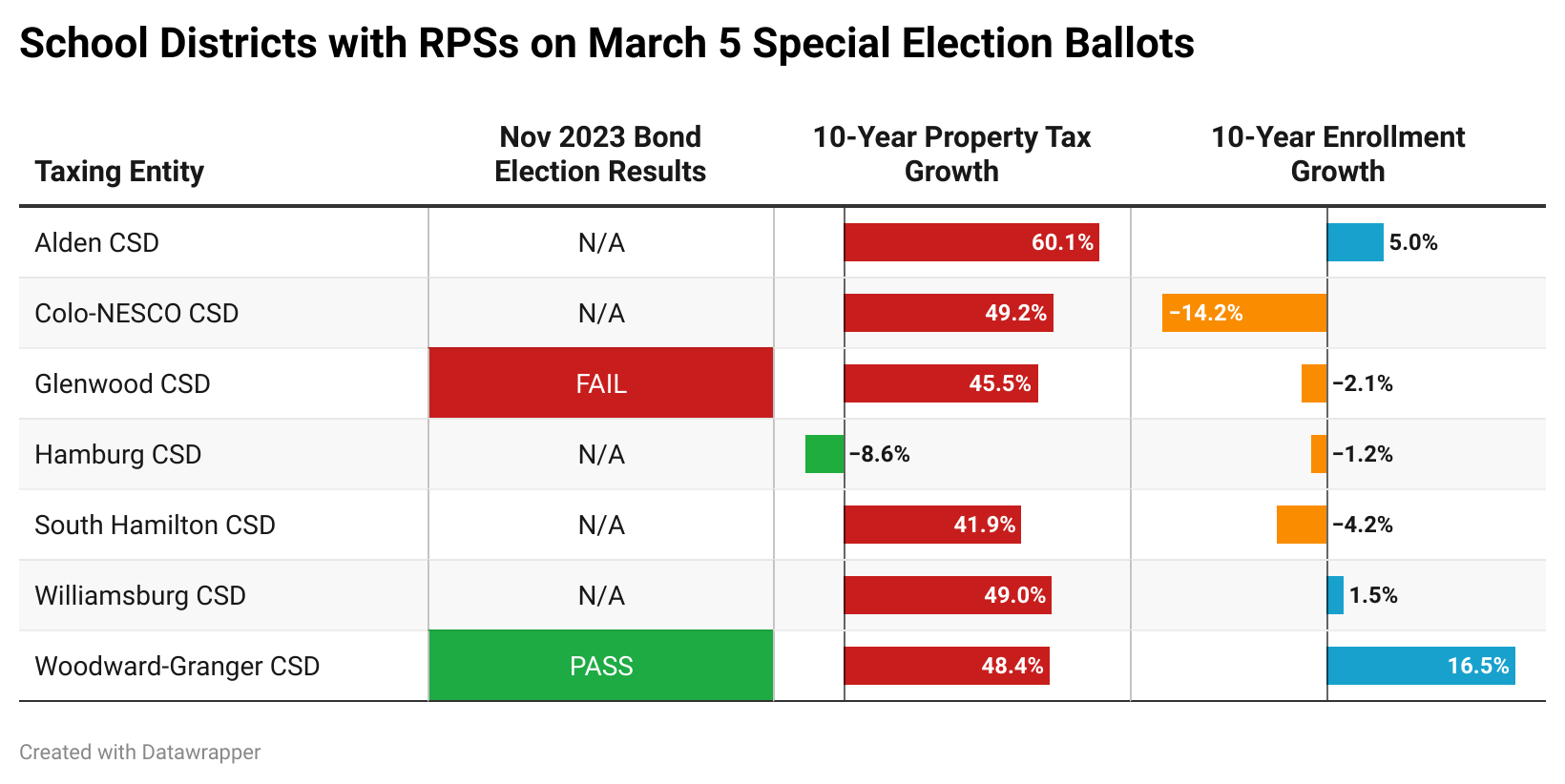

Glenwood CSD, for example, failed to win approval of a general obligation bond in November, and officials have been very open about their plan to leverage SAVE money to build some of the facilities voters turned down last fall. By using SAVE dollars this time around, they can bypass voter approval. Woodward-Granger CSD simply wants to extend its RPS because the current one is expiring. Meanwhile, Williamsburg CSD has listed examples of its past SAVE spending to imply how it will use funds moving forward.

The following table puts the seven pending RPS questions in context of whether the district placed a bond initiative on the November 2023 ballot as well as the growth (or decline) of local property taxes and student enrollment.

Misleading Comments by School Districts

Leading up to an election, school district officials attempt to make the case for their intentions, but their statements can sometimes be misleading.

The most common example is that “renewal of the district’s RPS will not lead to a property tax increase and will not extend an existing tax.” This is disingenuous because absent an RPS, the district’s property taxes would be decreased if all revenue bonds have been paid off. By enacting an RPS, the district extends its current property tax burden into the future. Variations on this misleading statement are that the RPS is “not endorsing a new tax burden” or that “the revenue generated has been used to meet our evolving needs while minimizing the burden on local taxpayers.”

Another misconception is that failure to approve an RPS means the district cannot access the SAVE funds. One example: “[we] ask voters to approve our Revenue Purpose Statement, a resolution necessary for districts to access sales tax revenue for a variety of purposes.” Districts receive SAVE funds with and without RPSs, it is only the use of those SAVE dollars that might be limited.

Revenue Purpose Statement Expiration

Legislation in 2019 set all RPSs voted on before July 1, 2019, to expire on January 1, 2031. For districts to continue spending SAVE funds as they wish, each must secure new RPSs approved by voters. Any new RPS will stay in effect through December 31, 2050, unless amended or repealed. For more information on the use of SAVE funds and Revenue Purpose Statements, click here.

Print a PDF

Print a PDF