Unassigned General Fund dollars beyond 15-30% of annual General Fund Expenditures might be excessive.

The concept of reserve funds and ending fund balances have been discussed by lawmakers and local officials alike in recent days at the Iowa Capitol and in the press. It’s something we’ve had our eyes on for years here at Iowans for Tax Relief Foundation. Following our brief summary of what an ending fund balance is and what it can or should be used for, we provide a comparison of the ending fund balances and expenditures in a number of communities across Iowa.

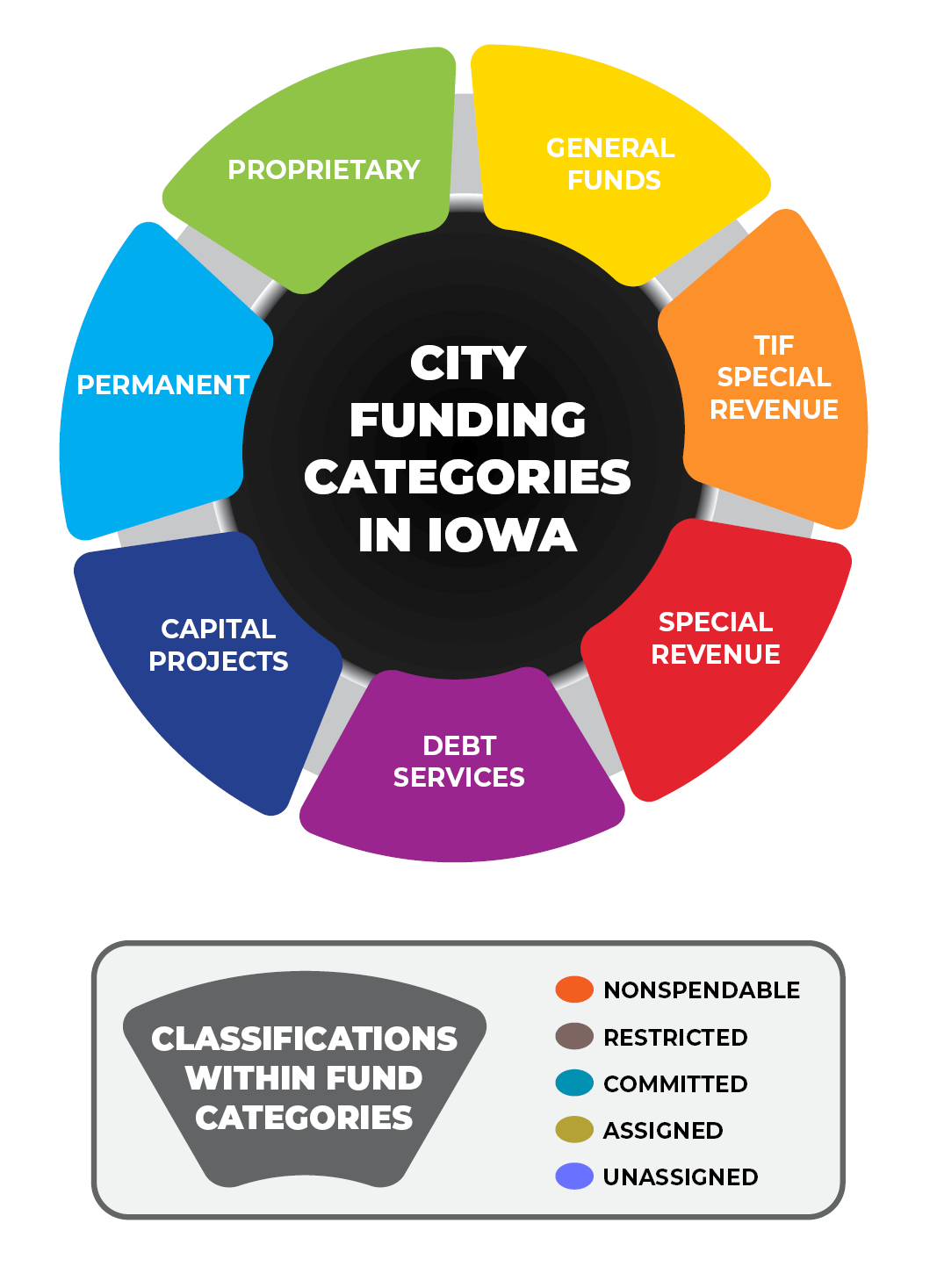

In local government finance, the ending balance can generally be understood as the sum total of revenue and expenditures over the lifetime of that particular unit of government. Essentially it’s the accumulation of operating surpluses that a city has been able to leave untouched and available for future use. In reality, it’s not quite that simple, though. Cities actually have seven different “funds” that revenue and expenses can be allocated to. And within each of those funds, there are five different classifications that define how a government is (or is not) constrained to use those dollars.

A certain amount of ending fund dollars, particularly Unassigned General Fund dollars, are appropriate to be carried over from year-to-year as a reserve. Different measures of good governance suggest a responsible and reasonable ending balance target for that classification would be somewhere between 15-30% of annual General Fund Expenditures. Unassigned General Fund dollars beyond that range might be considered excessive. The 40+ communities we researched combined to average an Unassigned General Fund balance that equaled 62% of their general expenditures.

Local governments typically aren’t restricted in how they can spend Unassigned General Fund dollars. They can use them to stabilize cash flow during the first few months of a fiscal year before property tax payments are received, and otherwise provide a cushion against unexpected expenditures or unforeseen dips in revenues. The link below is to a table which presents a cross section of communities across Iowa, detailing the Unassigned General Fund dollars as of June 30, 2022, the close of the most recent fiscal year.

Click here to view the Ending General Fund Balance Table

If your community isn’t included, you can go directly to the same source we utilized: 2022 Annual Financial Reports from Iowa Department of Management.

Print a PDF

Print a PDF