Iowa’s tax code is becoming more competitive, allowing individuals and businesses to flourish in a low-tax environment.

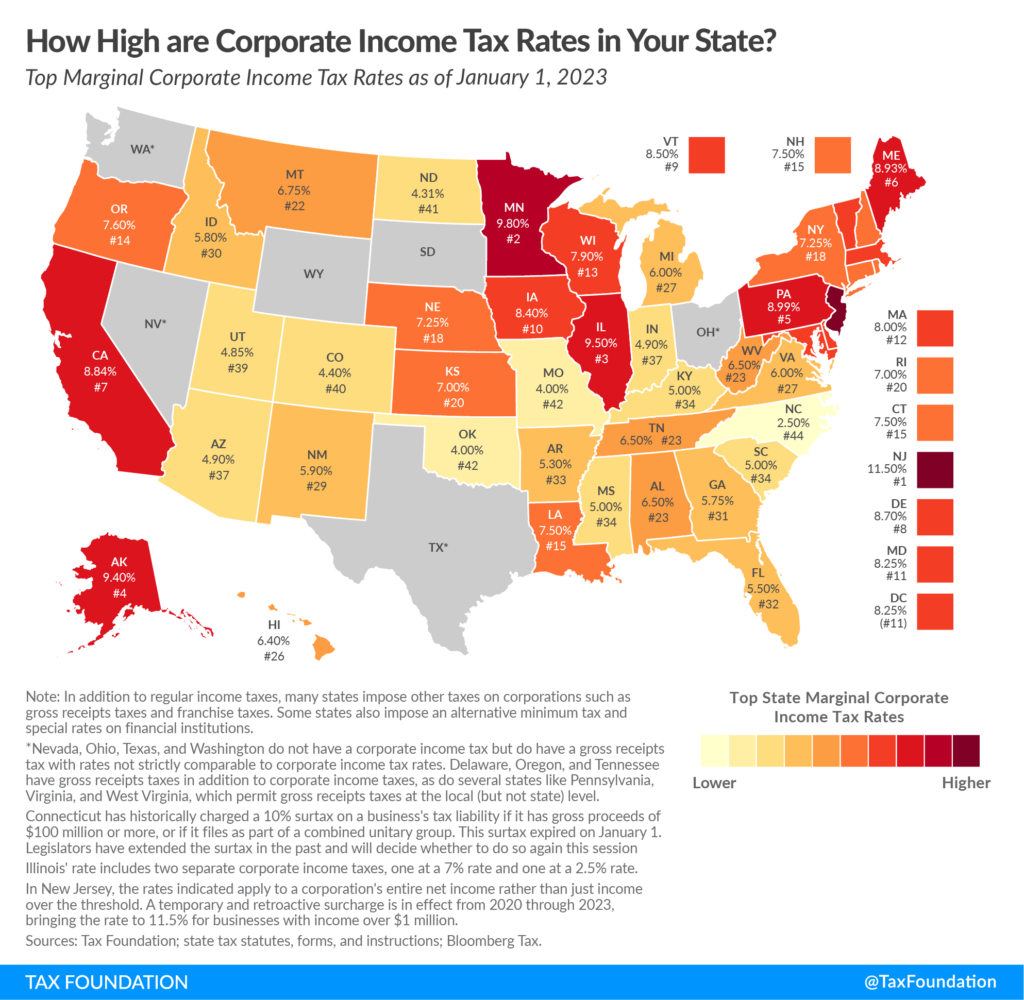

When Iowa’s corporate income tax was 12 percent, it was one of the highest in the nation. Starting on January 1, 2024, the top tax rate applied to corporations’ income will be lowered from its current 8.4 percent, which is still tenth-highest, to 7.1 percent.

Opponents attempt to cast lowering the corporate tax in a negative light, claiming it only benefits large corporations. To the contrary, the cost of high corporate tax rates is passed on to consumers, whereas the lower corporate tax rate will make Iowa more economically competitive, benefiting all taxpayers.

Source: Tax Foundation

Reduction of the corporate income tax rate has been part of Governor Kim Reynolds’s pro-growth reform agenda since 2018. Among other changes, Iowa’s historic 2022 tax reform law will begin to ratchet down the corporate tax rate to maintain a revenue target of $700 million per year. The ratchet will continue until Iowa reaches a single, flat corporate tax rate of 5.5 percent.

With corporate tax revenue exceeding $838 million in fiscal year 2023, the top rate will drop by a 15.5 percent increment.

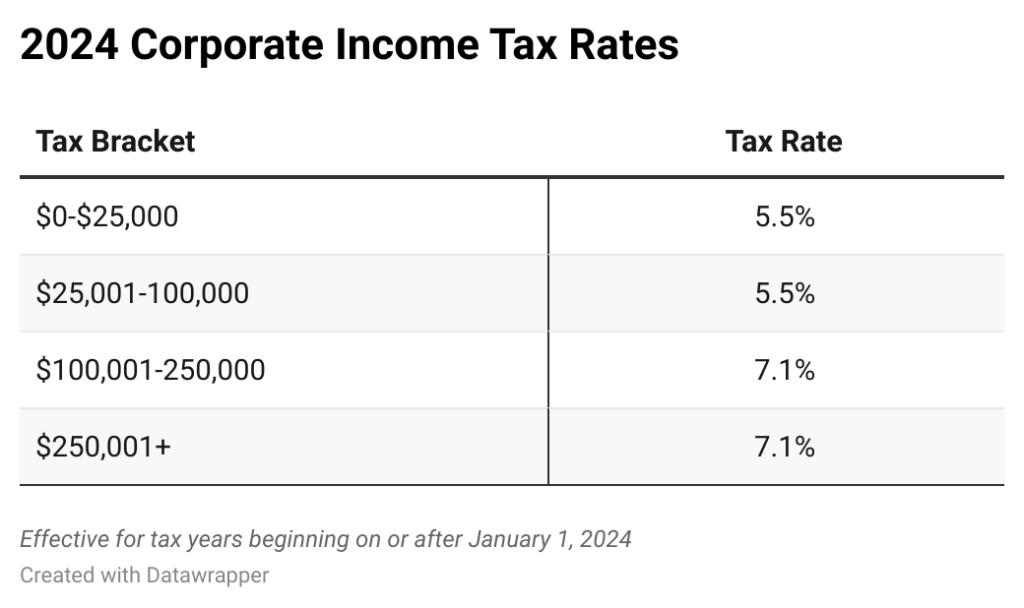

Effective for tax years beginning on or after January 1, 2024, the corporate income tax rates are as follows:

Source: Iowa Department of Revenue

Earlier projections did not anticipate the reform’s reaching this level until fiscal year 2027, but Iowa’s strong economy has accelerated progress. This rapid improvement results directly from the fiscally conservative policies of Governor Reynolds and the legislature. Conservative budgeting and prudent spending have, in turn, enabled pro-growth income tax rate reductions. Under current estimates, Iowa will achieve the 5.5 percent flat rate by fiscal year 2026, which is also when a 3.9 percent flat individual income tax will be fully implemented.

This virtuous ratchet works because income taxes punish growth, productivity, and investment, affecting the decisions and behavior of both businesses and individuals. High tax rates discourage work and investment and can trigger mass exodus of people and businesses from states that refuse to reform.

Naturally, the public tends to focus on individual income and property taxes, rather than corporate taxes, because people can see by their paychecks and property tax bills how their earnings and wealth are affected. In this regard, the corporate tax is silent, because its significant impact is understood mainly in board rooms and distributed across the economy. Economists Arthur Laffer, Stephen Moore, and Jonathan Williams explain that the effects of corporate taxes “are disguised as price increases, employment decline, out-of-state migration of businesses and individuals, and overarching restrictions of economic growth.”

Corporate taxes are also economically damaging because they “discourage business productivity by reducing the benefits of hiring workers or investing in infrastructure,” according to a joint study by the Tax Education Foundation of Iowa and the Buckeye Institute’s Economic Research Center. They “syphon resources away from productive investments and increase the cost of doing business.” Both business and labor are essential for economic growth, and high corporate tax rates discourage both.

“Compared to other major taxes, the corporate income tax is one of the most economically harmful taxes states levy, because while corporations are legally responsible for paying the tax, the economic incidence of the corporate income tax falls on a firm’s shareholders, employees, and consumers in the form of lower investment returns, lower wages, and higher prices,” wrote Katherine Loughead, a senior analyst with the Tax Foundation. Loughead notes that high corporate tax rates create a “sticker shock,” which can deter economic growth and investment.

With such concerns in mind, Laffer, Moore, and Williams suggest “states with corporate income taxes should aim for the lowest possible rate applied to all state corporations with no exceptions.” The last few years have found many states taking that advice and lowering both their individual and corporate tax rates. North Carolina has even placed its corporate tax on a path toward elimination. By 2030, its corporate tax will be eliminated.

Reforms don’t have to be that dramatic to be victories for all taxpayers. Iowa’s tax code is becoming more competitive, allowing individuals and businesses to flourish in a low-tax environment. Such flourishing can’t help but grow the economy, demonstrating that Iowa’s participation in the state “flat tax revolution” was the right course, and Governor Reynolds and legislative leaders have promised to continue moving Iowa forward.

Print a PDF

Print a PDF