Oklahoma wants to follow the Iowa playbook: controlling government spending is vital to a successful tax reform policy.

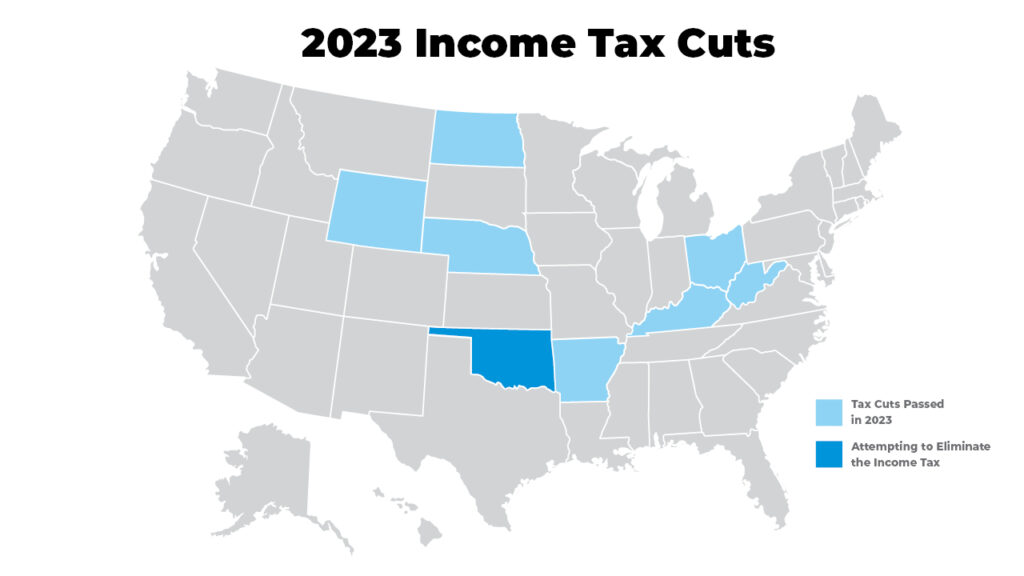

Oklahoma Governor Kevin Stitt has called a special legislative session, convening on October 3, 2023, for the purpose of income tax reduction and increased transparency within the state budget. The governor is not merely pushing for income tax relief but is asking the legislature to place the tax on a path toward elimination. If successful, Oklahoma would be the first state to take that step.

Arguing for income tax relief, Governor Stitt cites Oklahoma’s massive budget surpluses and reserves amounting to over $4.82 billion. The governor argues that Oklahoma needs to be more economically competitive, especially with its neighbor, Texas, among the states that never implemented an income tax to begin with. “We’re at 4.75 percent right now. Texas is at zero. And I want to lower our taxes, because when is the better time to do it,” he stated.

The design of his proposal has yet to be seen, but Governor Stitt has suggested it could be rolled out over the next decade. Income tax rates would fall based upon growth in revenue and, over a period of time, would match Texas’s zero percent.

The year 2023 has already seen another round of historic state-based tax reforms, including the following actions:

A crucially important feature of any tax reform is ensuring that spending is limited. In keeping with this principle, Oklahoma’s Governor Stitt is calling on the state legislature to complement tax reform with policy changes that would make the state budget more transparent and accountable to taxpayers. These reforms include, among others:

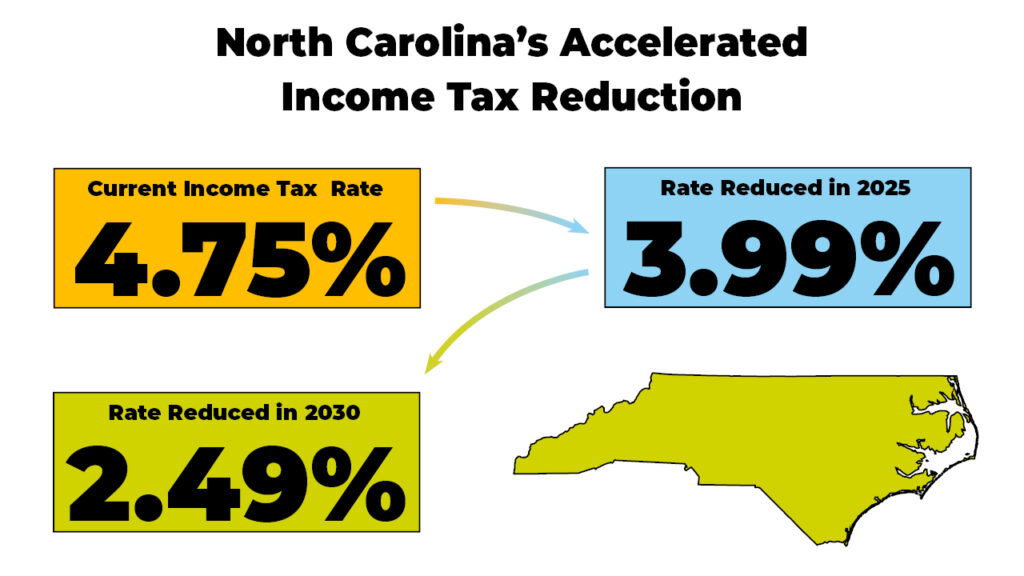

Looking beyond Oklahoma’s special session, state-level tax reforms look likely to continue. The North Carolina legislature has reached a budget compromise calling for the acceleration of income tax rate reductions. The current income tax rate of 4.75 percent will be reduced to 3.99 percent in 2025, and built-in revenue triggers will continue reductions to 2.49 percent. At that point, North Carolina will have the lowest flat tax in the nation, and its corporate tax is already on a path toward elimination by 2030.

In Iowa, Governor Kim Reynolds has stated repeatedly that our state is far from finished with tax reform. Her goal is to ensure Iowa has the lowest flat tax in the nation, perhaps even eliminating it. As the tax rates are already moving in that direction, Iowa is providing the important lesson that controlling government spending is vital to a successful tax reform policy. Early indications are that Governor Stitt is following in the same playbook.

Print a PDF

Print a PDF