Iowa taxpayers must be watchful for similar property tax relief deceptions. When it comes to public policy, the solution you’re sold doesn’t always provide the outcome you want.

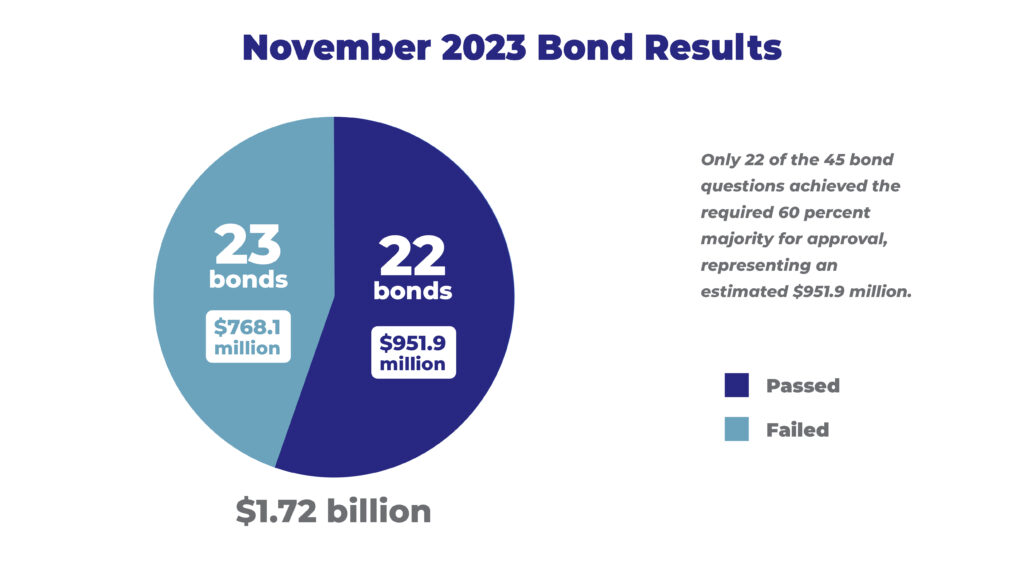

This past election was important for Iowa taxpayers. In addition to candidates for local government offices, Iowans voted on numerous bond proposals covering a variety of county, city, and school district projects. If all of the bond questions had passed, it would have meant $1.72 billion in new spending. During the election, only 22 of the questions achieved the required 60 percent majority for approval, representing an estimated $951.9 million. These results suggest taxpayers are paying more attention to bond questions owing to Iowans’ mounting frustration with high property taxes and recent legislation designed to increase participation.

As voters’ openness to budget and tax reforms continues, Iowa taxpayers should take a lesson from Colorado. As is true in many other states, Colorado struggles with high property taxes. Governor Jared Polis and the Democrats’ solution was a complicated ballot measure, Proposition HH. The proposal promised tax relief by lowering properties’ assessment rate in exchange for a revision of the state’s spending limitation, the Taxpayer Bill of Rights (TABOR). The resulting increase in spending would mostly be directed toward education, but a portion would also “backfill” local governments, ostensibly to take the pressure off of property taxes.

As it stands, Colorado’s TABOR is one of the strictest state-level spending limitations in the nation. It is “designed to limit the rate of growth in state revenue and spending to the sum of inflation plus the rate of growth in population while allowing a majority of voters to increase the revenue and spending limit when needed.” Surplus revenue under TABOR must be returned to taxpayers, and since its enactment, TABOR has refunded billions of dollars. In this context, Proposition HH’s promise of property tax relief was a deception, as Grover Norquist, President of Americans for Tax Reform, explained:

“While Prop HH would slightly reduce property tax rates and increase an existing exemption, those changes would not actually result in lower taxes. They would only result in faintly lower property tax increases this year before Prop HH would allow property taxes to grow at the same pace as property values. The fact is that Prop HH will result in massive and continued property tax hikes.“

Opponents suspect the real objective of Proposition HH was not property tax relief, at all, but the undermining of TABOR and unending increases in spending. Had it been enacted, Proposition HH could have led to a $20.9 billion statewide tax increase through 2040, even as property taxes continued to grow. “Prop HH — which would result in the largest tax increase in Colorado history — is not about lowering property taxes. It is a con intended to trick voters into damaging TABOR, which has protected Coloradans from taxing and spending increases for years,” stated Norquist.

Iowa taxpayers must be watchful for similar property tax relief deceptions. Many taxpayers are upset with rising property taxes and frustrated with local government officials’ excuses, but when it comes to public policy, the solution you’re sold doesn’t always provide the outcome you want. This past session, the legislature listened to their constituents’ demands for property tax relief and passed a comprehensive reform measure pointing Iowa in the direction of Colorado’s TABOR. Special interests are already scheming to turn this momentum in a direction that undermines our progress.

Key components of the bipartisan reform consolidate county and city property tax levies into the general levy, require stricter direct notification, and move bond elections to November. The new law also places a “soft cap” on the speed at which cities and counties can use tax rates to absorb increases in the assessed value of Iowans’ property.

For counties, the general basic county levy will have a maximum of $3.50 per $1,000 of taxable value, and the rural basic county levy maximum will be $3.95. The city general fund levy rate is set at $8.10. The “soft cap” then applies based on local valuation growth. If the valuation grows by 6 percent or higher, the taxable growth rate would be reduced by 3 percent. Valuation growth of 3 to 5.99 percent is reduced by 2 percent, while growth below 3 percent remains fully taxable. The new formula allows counties and cities below their general fund levy caps to increase rates, while those that exceed the max levy must bring the rates down to the maximum level.

Already, cities, counties, and local government subdivisions such as public libraries are proclaiming their budgets will have to be cut and urging their constituents to lobby legislators to revise the property tax law. In truth, the law does not limit budgets or spending, only how quickly they can grow to take advantage of property valuations. Yet, city, county, and school board officials will continue to pressure legislators during the 2024 legislative session to “reform” the law and water it down. Legislators may be tempted to relieve this pressure by shifting local budget responsibilities to the state’s general fund or using the Taxpayer Relief Fund to provide temporary relief by “buying down” the property tax school levy or transferring money in some other way.

Proponents of a scheme to use the Taxpayer Relief Fund to “buy down” the school property tax levy insisted it would result in direct property tax relief. Understood correctly, however, tax relief from the “buy down” would be temporary because it would rely on one-time money, creating a new obligation in the state’s general fund once the Taxpayer Relief Fund has been drained. The other insidious deception in the “buy down” idea is that it leaves local governments, including school districts, with no incentive to limit spending, and spending is the ultimate source of tax increases.

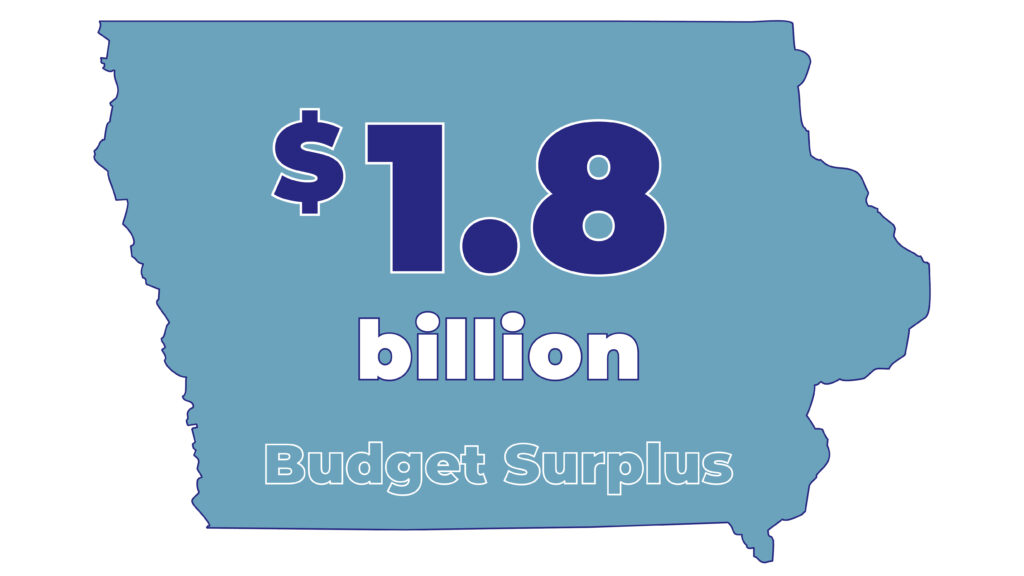

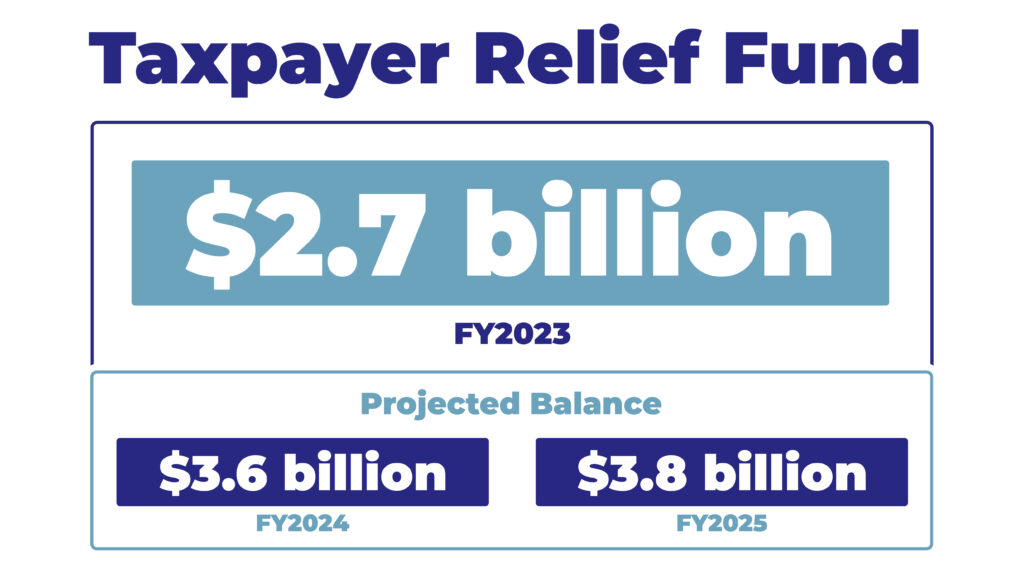

This is a lesson Iowans can learn — in a positive way — from the state government, which has been leading by example. For the last several years, Iowa’s budget has been in surplus as a result of conservative budgeting. The fiscal year 2023 surplus is $1.8 billion, which is $86 million higher than originally projected. Surpluses are projected, as well, for fiscal years 2024 and 2025. Meanwhile, the Taxpayer Relief Fund is increasing, with a current balance of $2.7 billion. This total is projected to increase to $3.6 billion in fiscal year 2024 and $3.8 billion in fiscal year 2025. In the spirit of its original intent, the Taxpayer Relief Fund should be dedicated to permanent and sustainable income tax relief. The large balance derives from the overcollection of income and sales taxes, not property taxes, and should be used to help individuals and small business owners keep more of their hard-earned income.

In exactly this way, the solution to crushing property tax increases begins with limiting local government spending. Local governments across Iowa should follow the budgeting example of Governor Kim Reynolds and the legislature. Under their guidance, state government has made difficult decisions, just as individuals, families, and businesses do every day, to restrain spending. Conservative budgeting, in turn, has made Iowa’s historic income tax reductions possible.

A local spending limitation could, for instance, limit spending or budget growth to 1 or 2 percent per year, with increases to be approved by voters during elections, requiring supermajorities. This approach would force local governments to justify their spending and provide taxpayers with protection against out-of-control budgets. The 22 successful questions during the recent bond election demonstrated that, if local government officials can demonstrate more spending to be necessary, voters will approve. Voters can — they must — be trusted in the formation of government policy, including budgets.

A large majority of Colorado taxpayers did not fall for the deception of Proposition HH. Nevertheless, Governor Polis, after calling a special session of the legislature, is working with Democrats to pass legislation that would accomplish the goals of Proposition HH. Colorado voters rejected Proposition HH, but TABOR may be undermined through the legislature. The outcome will be the same, that is, a weakened TABOR, more government spending, and limited property tax relief.

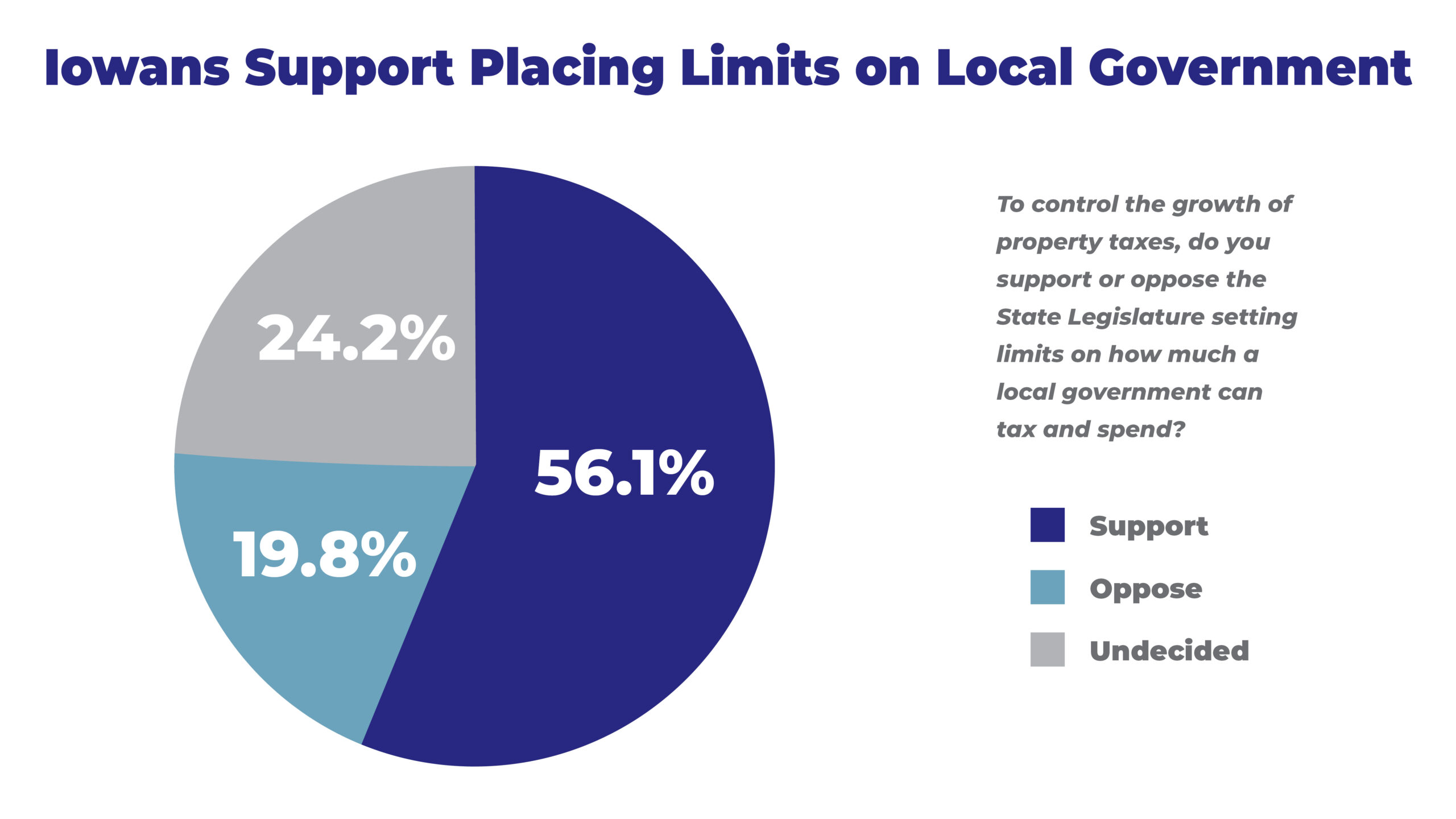

Similarly, a majority of Iowans, 56 percent, believe the legislature should place spending limits on local governments. The danger comes when spending increases are hidden behind deceptive property tax “relief” schemes. Iowa has a complex property tax system, and higher budgets can be slipped behind Taxpayer Relief Fund raids, shifts to the state general fund, or even new taxes that provide a portion of their collections for property tax relief.

The classic example of this possibility came in 1934, when, responding to pressure from the Great Depression and promising to provide property tax relief, the Iowa Legislature enacted its first sales and income taxes. The result was a gradual increase of all three taxes: property, sales, and income. Meanwhile, complex rules and exemptions that favor one taxpayer group, freezing or limiting the taxes it pays, makes the beneficiaries a special interest and buys them off. Regardless of the tax, if taxpayers want relief and lower rates, government at all levels must restrain spending.

Iowans are right to be angry and frustrated over high property taxes. Many Iowans feel that they are renting their home, place of business, or other property from local governments. This creates strong emotions, but as Coloradans figured out with Proposition HH, not all plans that play on these emotions are in the best interest of taxpayers. We must be wary of tricks and gimmicks, and we must make our voices heard by city, county, and school board officials to stop scheming and control their spending.

Print a PDF

Print a PDF