A strong, 2 percent cap on the growth of a local government’s property tax collections from year to year should be instituted by the state legislature.

Gas is expensive, the cost of groceries continues to rise, and insurance companies say they need to charge more because of the weather. Plus, because we live in Iowa, there’s another big-ticket item we all have to shell out our hard-earned dollars for: property taxes. Iowans are running out of room in our budgets when the spending spigots of local governments are left wide open. Fighting inflation at every step, too many of us have officials in our communities who keep demanding that families and businesses hand over increasingly more of their money in property taxes. These local government officials forget that taxpayers are also impacted by inflation and that the property tax dollars they are collecting come from Iowans.

This isn’t sustainable, but there is a way forward. It comes down to one simple step, a few schemes to avoid, and one pitfall to watch for. The simple step to solving the property tax problem is going directly to the source of the problem, local government spending, and limiting the amount your city and county can spend.

One Simple Step: Hard Cap on Property Tax Growth

A strong, 2 percent cap on the growth of a local government’s property tax collections from year to year should be instituted by the state legislature. Instead of monkeying with a solution that would get in the way of the market’s ability to drive property valuations, or an effort that aims to provide relief for one class of taxpayer at the cost of another, local governments in Iowa need to be put on a strict diet. New York and Texas, two states that couldn’t be farther apart on the political spectrum, both have a hard cap on the growth of local property taxes.

Local governments would be permitted reasonable budget increases and if they wanted to increase spending further, the spending cap could be superseded with a vote of the people. This would force local governments to justify why a spending increase is necessary. It would also prevent governments from collecting windfalls from assessment valuations.

One Scheme to Avoid: Sending State Dollars to Local Governments

In 2023, the legislature passed a comprehensive property tax reform law, which made some positive reforms. As the legislature considers further property tax reform local governments and special interests will likely do all they can to prevent a spending cap. Policymakers may also be tempted with the siren song of using the state General Fund to buy down property taxes or shift local government responsibilities back to the state.

Local governments cannot be allowed to look to Iowa’s legislators to subsidize their spending ambitions. State legislators have recognized the value in keeping the growth of Iowa’s spending reined in, and in turn they have been able to deliver four rounds of income tax cuts since 2018. To keep that progress going, the state will not be able take on the obligation of sending dollars back to local governments.

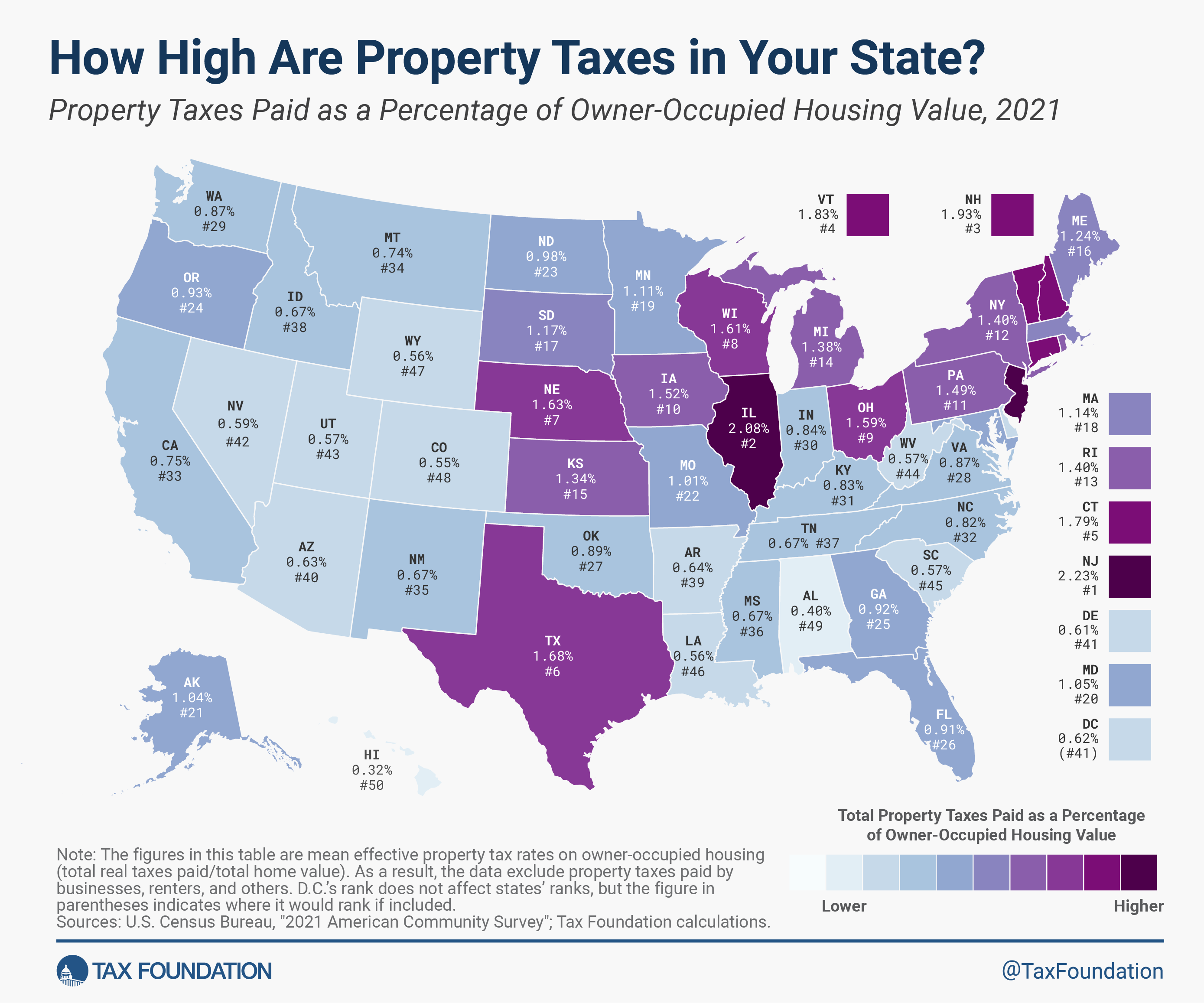

Tying state revenue to local property taxes is an experiment that has failed repeatedly. Iowa’s income taxes and sales taxes were instituted in 1934 in order to deliver property tax relief. 90 years later, Iowa’s property tax system is still ranked as one of the ten worst in the country.

A more recent example comes from 2022. After legislators shifted the responsibility of mental health services from counties to the state, nearly half of Iowa’s counties failed to pass on the savings to the taxpayer. It is clear that well-intentioned state support doesn’t create sustained tax relief. In addition, tax shifts or the state buying down property taxes without property spending limits will only result in temporary tax relief as local governments will continue to spend.

A spending limitation is only effective if it applies to the entire budget. The more line items that are exempt from a spending limitation will only make it more ineffective. Pressure will most certainly be applied by local governments to exempt certain spending categories from any budget cap. Applying the spending cap to the entire budget will be the only effective means of controlling local government spending.

One Pitfall to Watch For: Relying on Fee Income

In theory, government fees must be used to directly pay for the service for which the fee is being levied. In reality, local governments can get creative in their definitions and fees can start looking an awful lot like new taxes. Local governments can charge fees to recover the cost of a service. Nevertheless, local governments cannot charge excessive fees for the purpose of both covering the cost of a service and raising revenue. Trading lower taxes for higher fees has the same result: more dollars for government and fewer dollars for the taxpayer.

For too long, Iowans have voiced frustrations about their property tax bills that have fallen on deaf ears. Iowans complain about the cost of local government only to be handed a new bill even more expensive than the last. Now is the time to stop blaming assessors or shifting the burden to the state. Iowa needs to actually address the spending problem by instituting a 2 percent spending cap on local government budgets.

Print a PDF

Print a PDF{kind=link}