The American Legislative Exchange Council (ALEC) released the 13th edition of Rich States, Poor States: ALEC-Laffer State Economic Competitiveness Index. Rich States, Poor States, measures the competitiveness of each state in terms of economic outlook and performance. In the latest rankings, Iowa has moved from 29th to 25th in terms of economic performance, but in terms of economic outlook, Iowa has fallen from its 25th ranking in 2019 to 27th.

In recent years Iowa has been moving in a pro-growth direction with tax reform and prudent budgeting, but additional work needs to be done to make the state more competitive. Policymakers should continue to strive to create a more pro-growth tax code that is based on low rates and a broad base. “The data outlined in the 13th edition of Rich States, Poor States shows how economically competitive states thrive and how those that don’t make proactive pro-growth reforms, like Connecticut and Illinois, are left in the dust,” stated author and economist Dr. Arthur B. Laffer.

Tax rates matter for economic growth and competitiveness. Low taxes work as incentives while higher taxes discourage both productivity and growth. In fact one of the first principles of taxation is “when you tax something more you get less of it, and when you tax something less you get more of it.” For every dollar taken out in taxes, it is one less dollar that can be used to create additional economic activity or even given to charity.

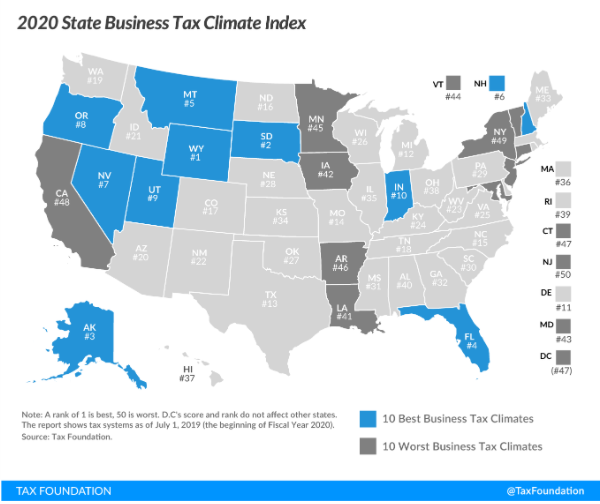

Iowa is in economic competition with 49 other states for both businesses and people. Jared Walczak, Vice President of State Projects at the Tax Foundation, noted that policymakers need to be concerned about losing economic activity to other states. “This means that state lawmakers must be aware of how their states’ business climates match up against their immediate neighbors and to other regional competitor states,” stated Walczak. In the Tax Foundation’s 2020 State Business Tax Climate Index, Iowa ranks in the top 10 for worst business tax climate (42 out of 50).

Iowa’s tax rates are some of the highest in our region. The top personal income tax rate is 8.53 percent while the top corporate income tax rate is 12 percent. High income taxes are the most harmful tax as they deter both economic growth and productivity. They are also the most volatile tax in economic downturns.

Pro-growth policies matter for a state to be competitive. States such as California, Illinois, New York, Connecticut, New Jersey, among others are plagued by the consequences of high tax rates and excessive spending policies. Many of these states are confronted with a massive fiscal crisis because of unsustainable pensions. The above-mentioned states are also the loudest voices calling for a massive federal government bailout to resolve their poor fiscal mismanagement.

Avoiding tax increases and controlling spending are not the only principles involved in enacting pro-growth tax policies. Following conservative revenue estimates and eliminating burdensome regulations are also essential. Iowa can look to several states as examples that have followed pro-growth and limited government policies to make their state more competitive.

Utah is perhaps the best example. For 13 years in a row, Utah has ranked number 1 in Rich States, Poor States for economic outlook. Utah has kept the top ranking because it has followed limited government policies by keeping tax rates, spending, and regulations at low levels. Utah’s Truth-in-Taxation is considered the most taxpayer friendly property tax law in the nation and has been instrumental in controlling the growth of property taxes.

Indiana and North Carolina are also improving their economic competitiveness by enacting pro-growth tax reforms. Indiana has gradually been reducing both their personal and corporate income tax, while North Carolina is considered the gold standard for state tax reform. North Carolina has demonstrated that controlling the growth of spending, lowering tax rates, adhering to conservative revenue estimates, and eliminating regulations are all possible.

Iowa is becoming more economically competitive and it is certain that COVID-19 will continue to create economic uncertainty. Nevertheless, policymakers in Iowa can continue to follow pro-growth policies that will not only benefit the taxpayer but make us even more competitive. Rich States, Poor States is a reminder that economic policies have consequences and why policies centered upon limited government principles will lead to greater freedom and prosperity.

Policymakers at the state and local level must avoid increasing taxes. This also means that spending must be controlled. Regardless of the tax, if spending is not controlled then tax relief will be next to impossible. Increasing taxes is a major policy mistake and it would not only hinder economic growth but punish Iowans who are already suffering from the impact of the pandemic. Iowa must continue to look for opportunities to further reduce tax rates.

In 2023, as part of the 2018 tax reform law, Iowa’s income tax is scheduled to be reduced to 6.5 percent. The caveat is, for the rate reduction to occur two stringent revenue triggers must be met. The first, state revenues must surpass $8.3 billion and the second, requires revenues to grow at least four percent during that fiscal year. The use of revenue triggers in state tax policy is a good idea, but creating a high threshold can unnecessarily delay tax rate reductions. The four percent growth trigger also places spending interests above those of the taxpayer.

")

The economic uncertainty may delay the 2023 rate reduction but repealing the 4 percent growth requirement would reduce a major roadblock to income tax relief.

In 2021, Iowa’s corporate tax rate is scheduled to be lowered from 12 percent to 9.8 percent. Also, Iowa will have three corporate tax rate brackets 5.5 percent, 9 percent, and 9.8 percent. Even at 9.8 percent, Iowa will still have a high corporate tax rate and many states have been lowering their corporate tax rates. Iowa should follow the example of Indiana and begin gradually lowering the corporate tax. This year Indiana lowered their corporate tax from 5.5 percent to 5.25 percent. Since 2012, Indiana has been gradually lowering the corporate tax rate from 8.5 percent, and the rate will continue to be lowered until it reaches 4.9 percent in 2022.

Increasing property taxes is also a major concern for Iowans. Even though property tax is utilized by local governments, the legislature can strengthen taxpayer protections to fight escalating property tax bills. The legislature could build upon the 2019 property tax transparency and accountability law by requiring local government to provide taxpayers with direct notification of a potential tax increase and how it would impact their property tax bill. Another policy solution would be requiring a spending limitation on local governments.

The Rich States, Poor States rankings are evidence, especially during this COVID-triggered economic downturn, that states need to follow pro-growth policies. “Sound tax policy and eliminating excessive government regulations continue to stand strong and true in improving states’ competitiveness, and we hope these states’ stories serve as a guide as we navigate the economic recovery following the COVID-19 pandemic,” noted Laffer.

Policymakers in Iowa should make tax rate reduction a policy priority. Lowering tax rates is never easy, but it is imperative. Rich States, Poor States has documented for over a decade that lower tax rates are key to economic competitiveness and growth.